Autumn 2026

March has arrived, and with that the weather starts to cool; this brings a fresh chapter and a chance to set your pace for the months ahead.

February delivered mixed signals for the Australian economy.

Labour market conditions were steady. The unemployment rate held at 4.1%, with 18,000 more people employed in January, driven by a rise in full-time jobs and partly offset by a fall in part-time roles.

Wage growth continued to edge higher, up 0.8% in the December quarter and 3.4% over the year, while household spending softened.

Inflation was slightly higher than expected, with CPI remaining at 3.8%, and trimmed inflation (the RBA’s measure of underlying inflation) increasing to 3.4%, up from 3.3%.

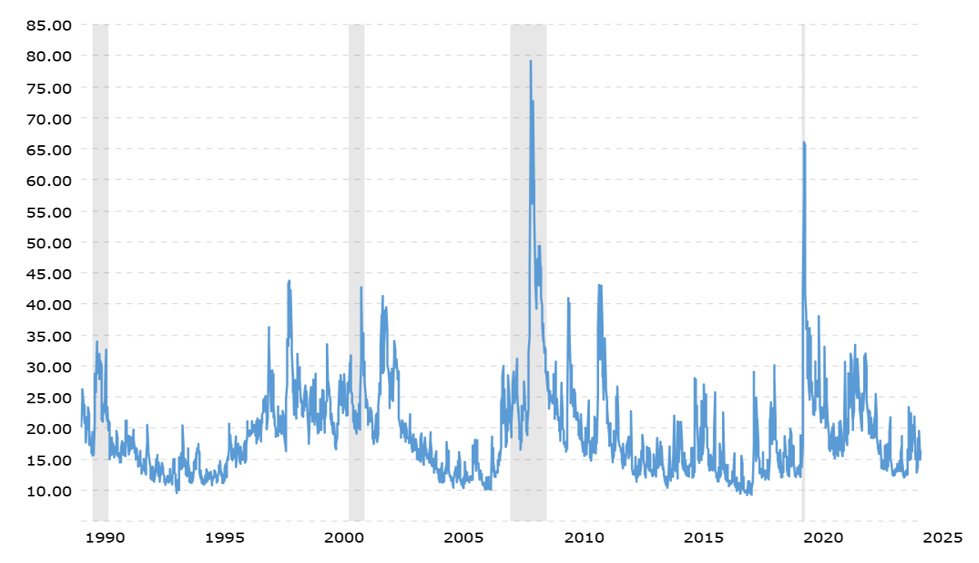

Reporting season added its usual volatility to the share market and the ASX hit several record highs towards the end of the month.

The Westpac–Melbourne Institute Consumer Sentiment Index fell further by 2.6% to 90.5 in February, impacted by February’s cash rate increase.

The Australian dollar strengthened, largely due to global risk sentiment, hitting a three-year high of USD 0.71 by month’s end.

The EOFY jobs that might matter more than you think

As the end of the financial year (EOFY) approaches, investors often focus on topping up super, maximising deductions, prepaying interest or reviewing portfolios. While these are all valuable activities, there are some less obvious tasks that can have a big impact on your tax position, wealth preservation and long-term planning outcomes.

Here are five areas that investors can often miss in EOFY planning.

1. Capital gains in volatile markets

Investment markets have been volatile in recent years, with rapid movements in equities, property and fixed income. When investors buy and sell during choppy market periods, capital gains tax (CGT) considerations become even more important.i

It is the ideal time to assess whether:

You should realise gains this year or defer them – The decision can hinge on:

- Expected income this year vs next year

- Whether you qualify for the 50 per cent CGT discount

- Available capital losses

- Investment timeframes and risk appetite

You have unused capital losses – Losses can be used to offset realised gains, but they cannot be used against ordinary income. Some investors may find that realising strategic gains before 30 June allows them to “unlock” unused losses that have been sitting dormant.

Be aware of “wash sale” rules. Some investors plan to sell an asset to realise a loss and then quickly buy it back. The ATO calls this a wash sale and may deny the loss.ii

2. Superannuation recontribution strategies

A super recontribution strategy is sometimes overlooked because it requires coordination between pension payments, contributions and tax components. But, when used appropriately, it may significantly reduce future tax for beneficiaries and increase flexibility in estate planning.iii

This strategy usually involves withdrawing a portion of your super (usually from the tax free and taxable components proportionally), then recontributing these funds back into super as a non-concessional contribution (if you’re eligible).

The result is that more of your balance becomes tax free, which can reduce or eliminate the “death benefits tax” that applies when super passes to non-dependent beneficiaries, such as adult‑children.iv

3. Bringing forward deductions and deferring income

While prepaying expenses and deferring income is a well-known EOFY strategy, it may not be successful for everyone, so check carefully that it’s useful for you.

Bringing forward deductions – You may be able toprepay, interest on investment loans, income protection premiums, ongoing advisory fees, and professional subscriptions. But if you’re approaching income thresholds (such as Medicare Levy Surcharge minimums, private health insurance rebates or HECS/HELP repayment bands) it’s important to calculate whether prepayments will actually deliver you a benefit.

Deferring income – Small businesses using cash accounting may be able to defer invoicing until July and investors might choose to delay receiving distributions or bonuses. But don’t forget that deferring income may affect borrowing capacity or government payments.

4. Managing Division 7A loans

Division 7A can catch business owners off guard at EOFY. These rules apply when a private company lends money, pays expenses or provides assets to shareholders or their associates. If not handled correctly, the ATO may treat the payment as an unfranked dividend, resulting in significant unexpected tax.v

To stay on top of your Division 7A obligations:

- Confirm all loans are documented

- Check minimum yearly repayments

- Consider whether to repay, refinance or restructure

- Don’t forget about company-paid personal expenses

A well-timed review can prevent unintended tax consequences and keep your structure compliant.

5. Reviewing your records

Another often missed EOFY task is checking that your records and substantiation are complete before preparing your tax return.

The ATO is increasing its use of data matching programs, so having accurate documentation is essential. This includes keeping receipts for deductible expenses and retaining statements for managed funds and other investments.

EOFY planning is about much more than topping up super or gathering receipts. Hidden traps like CGT and Division 7A timing can create unnecessary tax if ignored, while proactive strategies such as recontributions can deliver long-term estate planning benefits.

By taking a structured approach, you can ensure every part of your financial picture is working together, and no opportunity is missed. We’re here to help. Please give us a call.

ii Wash sales: The ATO is cleaning up dirty laundry | ATO

iii Super recontribution strategy: How it works | SuperGuide

iv Paying superannuation death benefits | ATO

v Loans by private companies | ATO

Tax Alert March 2026

ATO tightens compliance and expands employer support

The ATO has released several new resources, including a checklist to help employers get ready for what it calls a “once-in-a-generation change” along with an updated guidance on commercial deal tax.

Here’s a roundup of the latest news.

Preparing for Payday Super

The ATO has issued a Payday Super Checklist to help employers prepare for the commencement of the new regime from 1 July 2026.

The timeline checklist is designed to help employers understand the new requirements, plan their transition, prepare their business systems and processes and switch to paying super each payday.

In addition, Practical Compliance Guidelines outlining the ATO’s compliance approach during the Payday Super legislation’s first year of operation, have now been released.

Barter credit tax scheme under the microscope

The ATO is warning taxpayers to steer clear of an emerging tax scheme involving barter credits, a form of alternative currency used in some business networks.i

The scheme involves artificially inflating deductions by claiming donations of barter credits to deductible gift recipients. This practice is unlawful and may trigger a tax audit and significant penalties.

According to the ATO, the scheme is enabled by barter exchanges issuing credits with a nominal face value far higher than the amounts actually paid by participants.

Get certainty on commercial deals

To help business owners understand the tax implications of proposed commercial transactions, the ATO has created a series of case studies and videos.

The current case studiescover a range of scenarios, including a small business capital gains tax (CGT) rollover for a primary production business, the CGT implications when two siblings wish to sell family company shares to a third sibling, and the restructuring of a small company and subsequent share sale.

The information resources are designed to show how engaging early with the ATO can help resolve tax issues before lodgement and avoid later tax disputes.ii

Protect your GST and fuel tax credits

Some taxpayers are missing out on GST and fuel tax credits because they are not claiming the credits within the four-year time limit, which generally expires four years from the due date of the original BAS in which the credits should have been claimed.

Lodging an amendment or voluntary disclosure does not protect these credit entitlements, as the ATO must process amendments and include it in your tax assessment within the time limit.iii

Once GST and fuel tax credit entitlements expire, the ATO has no discretion to amend a tax assessment to include the credits. Good processes and regular reviews are essential to avoid missing out.

Avoiding delays when winding up SMSFs

The ATO is reminding trustees to follow the correct procedure when winding up their SMSF if they wish to avoid errors and delays.iv

Trustees have 28 days after lodging their final SMSF annual return (SAR) to complete the final rollover before the fund can be officially wound up. Failing to roll out all member benefits can result in significant delays, an inability to use SuperStream and requires lodgement of an additional SAR if assets remain after the wind-up date.

Trustees need to keep their contact details updated, promptly finalise outstanding transactions and pay debts, close the SMSF bank account only after confirming the wind-up, and roll over most of the fund’s asset before lodging the final SAR.

ATO help with natural disasters

Following the series of natural disasters around the country, the ATO is reminding taxpayers that support is available for those affected by disasters such as bushfires, cyclones, drought, flood or storms.v

For major disaster areas, the ATO may pause correspondence and provide extra support depending on circumstances. This may include:

- extra time to pay tax debts

- more time to lodge tax returns, BAS or other obligations

- personalised payment plans

- remission of penalties or interest charged during the affected period.

If you need more information or clarification about any of the recent tax changes, please give us a call.

i ATO warns about barter credit tax scheme | Australian Taxation Office

ii Commercial deals service resources | Australian Taxation Office

iii Act early: Protect your GST and fuel tax credit entitlements | Australian Taxation Office

iv Get it right! Avoid delays when winding up your SMSF | Australian Taxation Office

v Summary of our disaster support | Australian Taxation Office

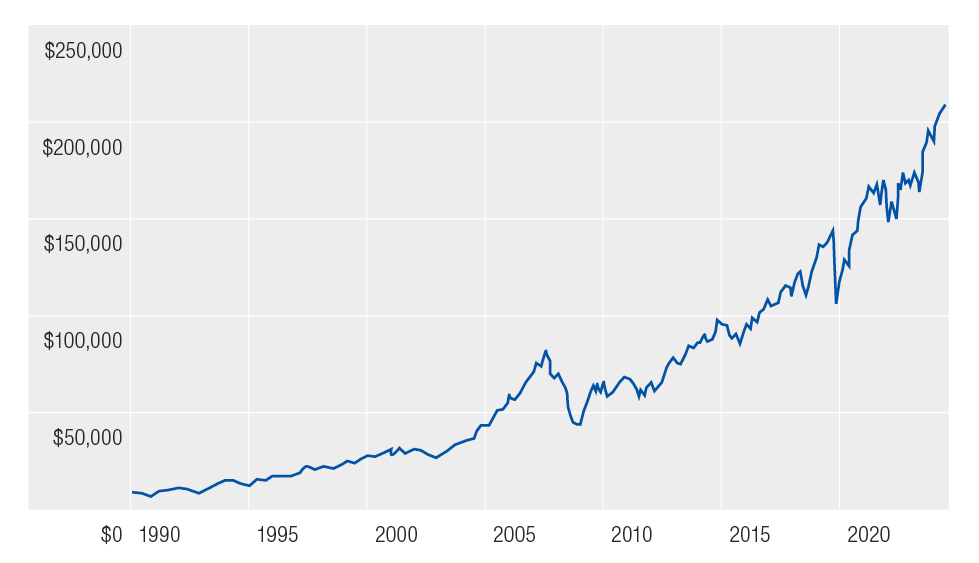

Warren Buffett: timeless lessons from a lifetime of investing

Warren Buffett has never looked much like a financial celebrity. He lives in the same house he bought in Omaha in 1958, prefers simple food, and has built one of the greatest investment records in history using his long-term value investing strategy.

Now stepping down at 95 years’ old from his role as CEO on the board of Berkshire Hathaway, one of America’s foremost holding companies, Buffett leaves behind a legacy that has earned him the enduring title of “the Oracle of Omaha.”

His story offers valuable lessons for anyone navigating markets, especially during times of uncertainty.

Time, patience, and the ability to change your mind

Perhaps Buffett’s greatest advantage was not a secret strategy or a rigid set of rules. It was time, combined with good judgment. He began investing as a teenager and stayed invested for more than seven decades. The power of compounding did much of the heavy lifting, but only because he stayed the course long enough to let it work.

As Buffett famously put it:

“Someone’s sitting in the shade today because someone planted a tree a long time ago.”

That long-term mindset helped him ignore short-term noise, particularly during market downturns. When markets fell, Buffett did not panic. He looked for opportunity.

“Be fearful when others are greedy, and greedy when others are fearful.”

But patience did not mean stubbornness. One of the most misunderstood aspects of Buffett’s success is the belief that he simply bought and held forever. In reality, he sold. He adapted. He exited investments when the facts changed. He acknowledged mistakes, sometimes very publicly, and moved on. Over time, entire sectors he once avoided were embraced, while others he once favoured were left behind.

“When the facts change, I change my mind. What do you do, sir?”

His real edge was not blind adherence to a philosophy, but the ability to apply principles flexibly. He knew when to stay invested, when to add, and when to walk away. That combination, long-term conviction paired with the willingness to change course, is far harder than following any checklist and far rarer in practice.

Staying calm when markets are down

Buffett’s calm during market stress has become legendary. He understood that volatility is not a flaw in markets. It is a feature of them. Declines were not signals to abandon investing altogether. They were moments that tested discipline and perspective and rewarded those able to separate temporary discomfort from permanent loss.

As Buffett succinctly observed:

“The stock market is a device for transferring money from the impatient to the patient.”

Importantly, his focus remained on underlying businesses and long-term outcomes, not daily price movements. That emotional discipline allowed him to act rationally when others could not, particularly during periods of widespread pessimism.

Investing in what you understand

Another cornerstone of Buffett’s approach was simplicity. He avoided businesses he could not understand and stayed within his “circle of competence.”

“Never invest in a business you cannot understand.”

This discipline kept him out of many speculative booms and fashionable trends. He was not trying to predict the next big thing. He was trying to make sensible decisions repeatedly over long periods of time, accepting that avoiding major mistakes can matter just as much as finding great opportunities.

A crucial caveat: context matters

While Buffett’s principles are powerful, his success is sometimes oversimplified. He invested with extraordinary scale, deep access, influence, and capital. He could survive mistakes that would permanently damage the average investor, negotiate unique deals, and wait far longer for outcomes to play out.

This means that while his thinking is broadly applicable – patience, discipline, and flexibility – his exact methods are not always transferable. Blindly copying concentrated bets or individual stock picks without those advantages can introduce risks that do not show up in hindsight success stories.

The real legacy

Warren Buffett did not succeed because he followed rules rigidly. He succeeded because he understood them well enough to know when to bend them, and when to abandon them entirely.

His legacy is not a list of stocks or a fixed formula. It is a reminder that successful investing is as much about judgment, adaptability, and emotional control as it is about time horizons or valuation metrics.

In that sense, Buffett’s greatest lesson is not “do what I did,” but “think carefully, stay patient, and remain willing to change when the world changes.”