Bonds are not usually the flashy upstarts of the investment world with their every move reported, like stocks.

But the Trump Administration’s extraordinary refashioning of world trade, with on-again off-again tariffs of eye watering amounts, has put bond markets in a similar position to share markets – in turmoil.

So, with the bond markets attracting more attention than usual, we take a closer look at the asset class.

What is a bond?

A bond is a bit like an interest-only loan and there are many different types of bonds available. A government (government bond), or sometimes a large company (corporate bond), issues bonds to investors to raise funds for infrastructure or, in the case of a company, for expansion.

Large institutional investors tend to favour some of the more complex types. Retail investors are more often interested in fixed-rate bonds, known as a fixed-income investment because of the regular payments made to the investor (or the coupon interest rate). The principal (called the face value) is repaid at an agreed date when the bond matures.

These bonds can also be traded on a secondary market by those who’ve chosen to sell their bonds before maturity. In this case, depending on the state of the markets and the economy, the amount they’re worth, or their capital value, may be higher or lower than the face value, which is fixed.

The most common fixed-rate bonds, issued by governments, are generally considered more stable. Nonetheless, all bonds are assigned a credit rating by independent rating agencies such as Standard & Poor’s or Moody’s.

Australia’s Commonwealth bonds, issued by the federal government, are AAA-rated reflecting strong fiscal management, economic stability and low default risk.i

State governments and quasi-government organisations such as the World Bank also issue bonds. The risk level for this category of bonds can vary.

Large companies, looking to expand or start new projects, often use bonds as a way to raise funds. Corporate bonds generally pay higher interest but are considered slightly more risky.

How to buy bonds

Investing in bonds can help to diversify a portfolio and provide a steady stream of income but for those with no knowledge or experience of the market, it is important to get quality professional advice and speak to us.

For example, if you had been relying on the conventional wisdom that bond markets are often up when share markets are down, recent share market activity would have delivered a shock. The usual flight to safety from share price volatility to bonds did not happen in the United States where, for a time, both markets were falling.

While it is possible to buy bonds directly when there is a public offer, it can be difficult for smaller individual investors to participate because of the large minimum transactions required.

Instead, most retail investors look to bond funds, bond exchange traded funds (ETFs) or managed funds for exposure to the bond market. The variety of funds on offer can help to diversify a portfolio by giving access to a range of different markets.

What affects bond rates?

Interest rate movements directly affect bond prices on the secondary market.

When interest rates rise, bond prices fall because newly issued bonds will be at the higher rate making older bonds less attractive and reducing demand.

Conversely, bond prices rise when interest rates fall because new bonds will offer the lower rates meaning there will be higher demand for older bonds, driving their prices up.

Bond prices are also influenced by economic conditions and investor sentiment.

Rising inflation can cause bond prices to rise while strong economic growth may decrease bond prices because investors often prefer to buy shares. Bonds with a lower credit risk, such as AAA-rated government bonds, tend to attract higher prices.

Be alert for scams

The Australian Securities and Investments Commission (ASIC) is warning investors about scammers using bond investments as a lure.ii

In one report earlier this year, scammers claimed to be offering sustainability investment bonds in Bunnings Warehouse.

The scam offered higher than market returns and claimed that investments are protected by the government. It included links to Bunnings genuine website although the company does not offer bonds or any investment products.

ASIC’s MoneySmart website warns that scammers often impersonate real companies. They may use the name of a real person working at the bank or company they say they represent.iii

“Be wary of surprise contact and independently verify who you are dealing with,” says ASIC. For detailed steps, see check before you invest.

If you would like to learn more about your options for investing in bonds, please give us a call.

How do bond yields change?

When bond prices fall, yields rise because the fixed coupon rate represents a higher percentage of the lower price. Similarly, when bond prices rise, yields fall because the fixed coupon rate is then a smaller percentage of the higher price.

For example, suppose interest rates fall. New bonds that are issued will now offer lower interest payments.

This makes existing bonds that were issued before the fall in interest rates more valuable to investors, because they offer higher interest payments compared to new bonds. As a result, the price of existing bonds will increase. However, if a bond’s price increases it is now more expensive for a potential new investor to buy. The bond’s yield will then fall because the return an investor expects from purchasing this bond is now lower.iv

Much of the 2025 Federal Budget was already known, after a volley of pre-election spruiking for votes. But Treasurer Jim Chalmers had one surprise up his sleeve – $17 billion in tax cuts. The first round of cuts will kick in on 1 July 2026 and second round on 1 July 2027, saving the average earner $536 each year when fully implemented.

With the next Federal Election due to be called any day, the Treasurer named five priorities for his fourth budget: helping with the cost of living, strengthening Medicare, building more homes, investing in education, and making the economy stronger.

He called it a plan for “a new generation of prosperity in a new world of uncertainty” that would help “finish the fight against inflation”.

The big picture

The Budget deficit has made an unwelcome, but not surprising, return. The Albanese government has been clear that we were headed back into the red and Treasurer Chalmers says the $42.1 billion deficit is less than what was forecast at both the last election and at the mid-year update.Gross debt has been reduced by $177 billion down to $940 billion, saving around $60 billion in interest over the decade.

Nonetheless, Australia is navigating choppy international waters with a “volatile and unpredictable” global economy.

Australia will feel the shockwaves from escalating trade tensions, two major global conflicts – in Ukraine and the Middle East, and slowing growth in China. Treasury predicts the global economy will grow by 3.25 per cent in each of the next three years in the longest stretch of below-average growth since the early 1990s.

However, Australia is in a good position to deal with the difficult conditions, the Treasurer says.

The Australian economy has “turned a corner” and continues to outperform many advanced economies.Inflation has moderated “significantly”, and the labour market has outperformed expectations. Meanwhile growth is predicted to increase from 1.5 per cent to 2.5 per cent by 2026-27.

Addressing the cost of living

With the rising cost of living expected to be central to the upcoming election campaign, the Budget aims to deliver more support to those doing it tough with further tax cuts, changes to Medicare and the Pharmaceutical Benefits Scheme (PBS), cuts to student debt and wage increases for aged care and childcare workers among a number of initiatives

Apart from the new tax cuts due in 2026 and 2027, the government will increase the Medicare levy low-income thresholds from 1 July 2024.

The energy bill relief is also being extended to the end of this year. At a cost of $1.8 billion, every household and around one million small businesses will each receive $150 off their electricity bills in two quarterly payments.

The government claims that energy bill relief has helped to drop electricity prices by 25.2 per cent across 2024.

Students aren’t forgotten in the Budget with a cut of $19 billion in student loan debt, with all outstanding student debts reduced by 20 per cent and a promised change to make the student loan repayment system fairer.

The government is tackling the cost of living where it’s often most obvious – at the cash register. It is providing support for fresh produce suppliers to enforce their rights and will make it easier to open new supermarkets. It’s also planning to focus on “unfair and excessive” card surcharges.

Looking for a clean bill of health

Almost $8 billion will be spent to expand bulk billing, the largest single investment in Medicare since its creation 40 years ago.

Treasurer Chalmers says nine-out-of-10 GP visits should be bulk billed by the end of the decade with an extra 4,800 bulk billing practices.

There’ll also be another 50 Urgent Care Clinics across the country, taking the total to 137, and public hospitals will get a boost of $1.8 billion to help cut waiting lists, reduce waiting times in emergency rooms and manage ambulance ramping.

Cheaper medicines

The cost of medicines is also in the government’s sights. The maximum cost of drugs on the Pharmaceutical Benefits Scheme (PBS) will be lowered for everyone with a Medicare Card and no concession card. From 1 January 2026, the maximum co-payment will be lowered from $31.60 to $25.00 per script and remain at $7.70 for pensioners and concession cardholders. Four out of five PBS medicines will become cheaper for general non‑Safety Net patients, with larger savings for medicines eligible for a 60‑day prescription.

An extra $1.8 billion is also being invested to list new medicines on the PBS.

Increasing the housing stock

The government’s previously announced target of 1.2 million new homes over five years has seen 45,000 homes completed in the first quarter.

The budget sees an extra $54 million to encourage modern construction methods and $120 million to help states and territories remove red tape.

With building set to increase, more apprentices are needed, and the government has announced financial incentives of up to $10,000 to encourage more people to take up apprenticeships in building trades. Some employers may also be eligible for $5,000 incentives for hiring apprentices.

The Help to Buy program that allows homebuyers to get into the market with lower deposits and small mortgages will be expanded with an extra $800 million to lift property price and income caps to make the scheme more accessible.

To help increase housing stock available, foreign buyers will be banned from purchasing existing dwellings for two years from 1 April 2025. Land banking by foreign owners will also be outlawed.

Recovering and rebuilding

The damage from ex-Tropical Cyclone Alfred and subsequent rains in Queensland and northern New South Wales is so extensive that it is expected to wipe a quarter of a percentage point off quarterly growth.

Flooding has damaged infrastructure and disrupted supply chains, agricultural production, construction, retail, and tourism activity.

The government expects costs of at least $13.5 billion in disaster support. As a result, the Budget includes $1.2 billion to be placed in a contingency fund to better respond to future disasters.

Looking ahead

Despite concerning events on the world stage, Australia’s economy is emerging “in better shape than almost any other advanced economy”.

Inflation and unemployment are coming down and wage growth will be stronger. To help underpin continuing economic growth, the Budget adds $22.7 billion to the government’s Future Made in Australia agenda.

It includes extra investment in renewable energies and low emissions technologies and an expansion of the Clean Energy Finance Corporation. The plan also includes more than $15 billion in support for private investment in hydrogen and critical minerals production, clean energy technology manufacturing, green metals, and low carbon liquid fuels.

And, as the trade war kicks off, the Budget allocates $20 million to a Buy Australian campaign.

“The plan at the core of this Budget is about more than putting the worst behind us. It’s about seizing what’s ahead of us,” the Treasurer says.

If you have any questions about the Budget measures announced, please don’t hesitate to contact us.

Information in this article has been sourced from the Budget Speech 2025-26 and Federal Budget Support documents. It is important to note that the policies outlined in this article are yet to be passed as legislation and therefore may be subject to change.

As we say goodbye to the heat of summer, we can look forward to enjoying the cooler days ahead. Along with the drop in temperature, the RBA brought much relief to mortgage holders and dropped the cash rate by 25 basis points in February. The cash rate is now sitting at 4.10 per cent following the first rate-reduction since November 2020.

Inflation remained steady in February, at 2.5 per cent and core inflation at 2.8 per cent; however, the RBA remains cautious and has not guaranteed further cash rate cuts in 2025. Some economists are predicting further cuts in 2025, but time will tell.

While there is ongoing tension between Russia-Ukraine and the Middle East, and a looming trade war due to Trump’s proposed tariffs, the global economic outlook continues to remain unpredictable.

US markets reacted to the lower-than-expected consumer spending and continued geopolitical issues, with another month of volatility.

It’s also been volatile on the Aussie share market, with the ASX 200 losing ground earlier in the month, bouncing back to reach an all-time high, only to start falling again to close at it’s lowest point in two months.

A similar pattern has been happening with the Aussie dollar, reaching a high of $0.64US cents mid-February, then losing momentum, and now hovering around $0.62US cents.

Turbocharge your super before 30 June

More than half of us set a new financial goal at the beginning of 2025, according to ASIC’s Moneysmart website. While most financial goals include saving money and paying down debts, the months leading up to 30 June provide an opportunity to review your super balance to look at ways to boost your retirement savings.

What you need to consider first

If you have more than one super account, look at consolidating them to one account. Consolidating your super could save you paying multiple fees and it will be easier to keep track of.

When transferring super into one account, do your homework and shop around, your current fund may not be your best option.i

How to boost your retirement savings

Making additional contributions on top of the super guarantee paid by your employer could make a big difference to your retirement balance thanks to the magic of compounding interest.

There are a few ways to boost your super before 30 June:

Concessional contributions (before tax)

These contributions can be made from either your pre-tax salary via a salary-sacrifice arrangement through your employer or using after-tax money and depositing funds directly into your super account.

Apart from the increase to your super balance, you may pay less tax (depending on your current marginal rate).ii

Check to see what your current year to date contributions are so any additional contributions you may make don’t exceed the concessional (before-tax) contributions cap, which is $30,000 from 1 July 2024.iii

Non-concessional contributions (after tax)

This type of contribution is also known as a personal contribution. it is important not to exceed the cap on contributions, which is set at $120,000 from 1 July 2024.iv

If you exceed the concessional contributions cap (before tax) of $30,000 per annum, any additional contributions made are taxed at your marginal tax rate less a 15 per cent tax offset to account for the contributions tax already paid by your super fund.

Exceeding the non-concessional contributions cap will see a tax of 47 per cent levied on the excess contributions.

If you’ve had a break from work or haven’t reached the maximum contributions cap for the past five years, this type of super contribution could help boost your balance – especially if you’ve received a lump sum of money like a work bonus.

These contributions are unused concessional contributions from the previous five financial years and only available to those whose super accounts are less than $500,000.

There are strict rules around this type of contribution, and they are complex so it’s important to get advice before making a catch-up contribution.

Meanwhile, the fate of a proposed new tax, known as Division 296, applying to super balances over $3 million is still unknown. It has yet to be debated and go to a vote in the Senate.

Downsizer contributions

If you are over 55 years, have owned your home for 10 years and looking to sell, you may be able to make a non-concessional super contribution of as much as $300,000 per person – $600,000 if you are a couple. You must make the contribution to you super within 90 days of receiving the proceeds of the sale of your home.

Spouse contributions

There aretwo ways you can make spouse super contributions, you could:

split contributions you have already made to your own super, by rolling them over to your spouse’s super – known as a contributions-splitting super benefit, or

contribute directly to your spouse’s super, treated as their non-concessional contribution, which may entitle you to a tax offset of $540 per year if they earn less than $40,000 per annum

Again, there are a few restrictions and eligibility requirements for this type of contribution.

Get in touch for more information about your options and for help with a super strategy that could help you achieve a rewarding retirement.

New year, new rules: ATO’s 2025 focus areas for small businesses

The Australian Taxation Office has kicked off 2025 by announcing its major areas of interest when it comes to small businesses. It has also highlighted a tougher stance when it comes to super guarantee (SG) compliance and GST fraud. Here’s a roundup of the latest tax news.

deductions and concessions (non-commercial losses and small business CGT concessions)

incorrect use of business income (business money and assets used for personal use of benefit), and

businesses operating outside the system (GST registration and income for taxi, limousine and ride-sourcing services).

The ATO intends to review and publish quarterly focus themes to help small businesses work on fixing issues in these areas.

GST fraud warning

The ATO-led Serious Financial Crime Taskforce is warning businesses against trying to cheat the tax and super system by committing GST fraud, saying it is on the lookout for potentially fraudulent activities.i

New information shared between government agencies shows some businesses are using complex financial arrangements to disguise transactions with the aim of obtaining larger GST refunds.

The arrangements include false invoicing between related entities, deliberately misaligning GST accounting methods across a group, duplicating GST credit claims, and claiming for fake purchases.

Tax penalties increase

The cost of penalty units imposed by the ATO if you fail to meet your tax obligations has increased again, rising from $313 to $330 per penalty unit.ii

The new rate applies to infringements occurring on or after 7 November 2024. For example, the penalty for failing to keep or retain tax records as required is 20 penalty units (20 units x $330 = $6,600).

Other penalties apply to missed and late SG payments, individual and corporate SMSF trustees and GST when buying or selling new residential premises.

SG compliance under scrutiny

With more timely data now available from Single Touch Payroll reporting, SG reporting and payments have become a priority area for the ATO. It is reminding employers to keep good records, report accurately and pay their obligations on time.

As part of its firmer response towards non-payment of SG contributions, the ATO issued 8,710 director penalty notices relating to 6,500 companies during 2023-24.iii

Although the regulator found 92.4 per cent of employers paid their SG obligations without intervention, it still collected and paid $932 million in SG entitlements into the super accounts of 797,000 employees.

GST and fuel tax credit time limits

The ATO is encouraging businesses eligible for GST and fuel tax credits to claim their credits within four years of the due date of the earliest Business Activity Statement (BAS) where a claim could have been made.

Once the time limit passes, you are no longer eligible to claim the credits. Lodging an amendment to an original assessment or requesting a private ruling are not considered as claiming.

Old credits can be claimed in your next BAS (provided it is within the eligibility period), by lodging a revised BAS for the original period via ATO Online Services, or by lodging a valid objection during the time limit to preserve your entitlement to the credits.

Change to myGovID

The Australian Government’s digital ID app myGovID, used to access government services, has been renamed myID.

The app provides secure access to government services using your existing login details (including email address), with the identity strength remaining the same. Existing app users should find the app automatically updated on their smart device, or it can be manually updated from the Apple app store or Google Play.

The ATO is warning users that scammers are seeking to take advantage of the name change. Any message or email asking you to set up a new myID or reconfirm your details is a scam.

From the economy bending policies of Trump 2.0 to the growing strength of the far right in Europe, the new alliance between Russia and the United States, the wars in Ukraine and the Middle East, and the US President’s vow to upturn world trade rules, the markets are certainly navigating tricky times.

In recent months we’ve seen volatility in some areas but cautious optimism in others in a reflection of the hand-in-glove relationship between politics and markets.

Of course, economic policies, laws and regulations– think tax increases or decreases, new business regulations or even referendums – have a big effect on how investors allocate their portfolios and that impacts market performance.

In 2016, when the United Kingdom voted to leave the European Union, the UK pound plunged and more than US$2 trillion was wiped off global equity markets.i

In the following four years until Brexit was finally achieved in 2020, the FTSE 100 performed poorly compared to other markets as domestic and international investors looked elsewhere to avoid risk. While it has risen since a massive drop during the coronavirus pandemic, the exodus of companies from the London Stock Exchange continues with almost 90 departures in 2024.ii

Interest rate movements and any hint of political instability can also bring about a sell off or a rally in prices, with companies holding off on capital investment and causing economic growth to slow.iii

Global oil prices rose 30 per cent in 2022 when Russia invaded Ukraine causing European stock markets to plunge 4 per cent in a single day.iv Since then, oil prices have fluctuated and are now back to pre-war levels and gold has reached new heights as investors globally look for a safe haven from high geopolitical risks.

Do elections have an effect?

Elections, which almost always cause market disruptions during the uncertainty of the campaign period and shortly after the vote is known, have featured strongly in the past six months or so.

A review of 75 years of US market data has found that, while there may be outbursts of volatility in the lead up to the vote, there’s minimal impact on financial market performance in the medium to long term. The data shows that market returns are typically more dependent on economic and inflation trends rather than election results.v

Nonetheless, the noisy 2024 US Presidential campaign saw some ups and downs in markets during the Democrats’ upheaval and the switch to Kamala Harris as candidate. Donald Trump’s various policy announcements on taxes, immigration, government cost cutting and tariffs both buoyed and dismayed investors.

Analysis by Macquarie University researchers of the three days before and after election day found significant abnormal returns in US equities immediately after the vote.vi

But the surge was short-lived as investor sentiment fluctuated. Small cap equities with more domestic exposure experienced the highest returns while the energy sector also saw substantial gains, in anticipation of regulatory changes.

While currently the S&P500 and the Nasdaq have both gained overall since the election, there’s been extreme share price volatility.

How Australia has fared

Meanwhile, any impact on markets ahead of Australia’s upcoming federal election has so far been muted thanks to the volume of world events.

The on-again off-again US tariffs are causing more concern here for both policymakers and investors. Tariffs on our exports could mean higher prices and a drop in demand for our goods and services, leading to economic uncertainty.

In early February, the Australian share market took a dive immediately after President Trump’s announcement of tariffs on Mexico, Canada and China, wiping off around $50 billion from the ASX 200. They recovered slightly only to fall again later as the Reserve Bank cut interest rates. In the US, some tech companies delayed or cancelled their listing plans because of the volatility and uncertainty caused by the announcements.vii

Amid a turbulent start to 2025, most economists agree the markets are unlikely to hit last year’s 7.49 per cent achieved by the S&P ASX 200.

Reserve Bank of Australia governor Michele Bullock is similarly downbeat on the prospects for the year, saying uncertainty about the global outlook remains “significant”.viii

Please get in touch if you’re watching world events and wondering about the impact on your portfolio.

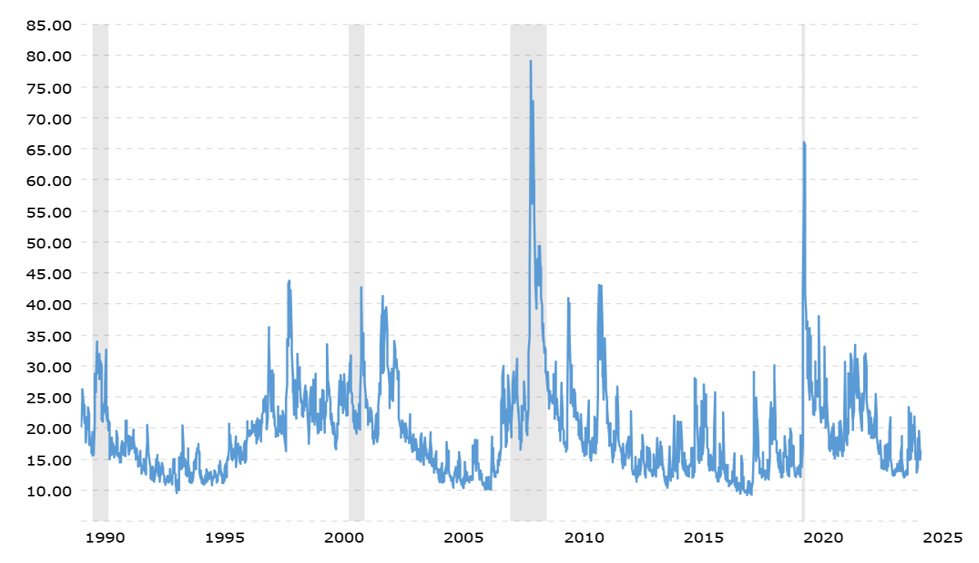

As investors grapple with uncertainty, keeping a cool head has never been more important.

“Time in the market, not timing the market” is a popular investment philosophy that emphasises the importance of staying invested over the long term rather than trying to predict short-term market movements. While markets can be volatile in the short term, historically, they tend to grow over time.

It’s a strategy that helps you avoid getting caught up in short-term market fluctuations or trying to predict where the market is heading.

With the recent market turbulence, from the global effects of US President Donald Trump’s administration to ongoing conflicts in Ukraine and the Middle East, savvy investors look beyond the immediate chaos to focus on strategies that encourage stability and growth over the long-term.

It’s a hallmark of the approach by the world’s most high-profile investor, Warren Buffet, who argues that short-term volatility is just background noise.

“I know what markets are going to do over a long period of time, they’re going to go up,” says Buffet.i

“But in terms of what’s going to happen in a day or a week or a month, or even a year …I’ve never felt it was important,” he says.

VIX Volatility Index – Historical Chart – 1990 -2025

Source: Macrotrends

Buffet first invested in the share market when he was 11 years old. It was April 1942, just four months after the devastating and deadly attack on Pearl Harbour that caused panic on Wall Street. But he wasn’t fazed by the uncertain times.

Today Buffet is worth an estimated US$147 billion.ii

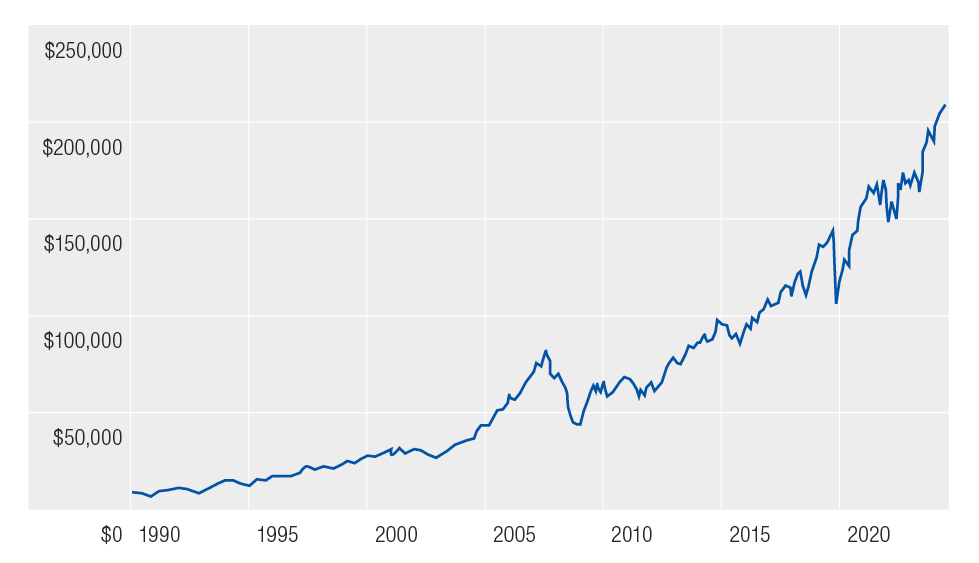

Long-term growth in Australia

While growth has been higher in the US, investors in Australian shares over the long-term have also fared well. For example, $10,000 invested 30 years ago in a basket of shares that mirrored the All Ordinaries Index would be worth more than $135,000 today (assuming any dividends were reinvested).iii

And it’s not just the All Ords. If that $10,000 investment was instead made in Australian listed property, it would be worth almost $95,000 today or in bonds, it would be worth almost $52,000.

Australian shares – tracking performance from 1990 to 2024

Source: Vanguard

In real estate, the average house price in Australia 30 years ago was under $200,000. Today it is just over $1 milllion.iv

Meanwhile, cash may well be a safe haven and handy for quick access but it is not going to significantly boost wealth. For example, $10,000 invested in cash 30 years ago would be worth just $34,000 today.v

Diversify to manage risk

Diversifying your investment portfolio helps to manage the risks of market fluctuations. When one investment sector or group of sectors is in the doldrums, other markets might be firing, therefore reducing the chance that a downturn in one area will wipe out your entire portfolio.

For example, the Australian listed property sector was the best performer in 2024, adding 24.6 per cent for the year. But just two years earlier, it was the worst performer, losing 12.3 per cent.vi

Short-term investments – including government bonds, high interest savings accounts and term deposits – can play an important role in diversifying the risks and gains in an investment portfolio and are great for adding stability and liquidity to a portfolio.

Ongoing investment strategies

Taking a long-term view to accumulating wealth is far from a set-and-forget approach and by staying invested, you give your investments the best chance to grow, avoiding the risks of missing out on key growth periods by trying to time your buy and sell decisions perfectly.

Reviewing your investments regularly helps to keep on top of any emerging economic and political trends that may affect your portfolio. While it’s important to stay informed about market trends, it is equally important not to overreact when there is volatility in the share market.

Emotional investing can lead to poor decisions, so remember the goal is not to avoid market declines but to remain focussed on your overall long-term investment strategy.

Please get in touch with us if you’d like to discuss your investment options.

Welcome to summer and, for many, an active season with last-minute tasks and celebrations with family and friends. We take this opportunity to wish you and your family a joy-filled and safe festive season!

While headline inflation eased to 2.8% in the September quarter, the Reserve Bank remains unmoved on interest rates. RBA Governor Michelle Bullock says the drop in the cost of living may be welcome relief for most of us, but the Board’s measure to watch is trimmed mean inflation and that’s still not “sustainably” in the desired target range of 2-3%. It’s not likely to get there until late in 2026, the RBA predicts.

The sharemarket reacted sharply to the Governor’s comments in the last days of a month that had seen several all-time highs. US President-elect Donald Trump’s promise for 25% tariffs on Canadian and Mexican goods also contributed to the billion dollar shares sell-off. Nonetheless, the S&P ASX200 finished November 3.4% higher.

The Australian dollar is also taking a beating from the possibility of both the US tariffs and the RBA’s rates forecast. It hit a seven-month low below 65 US cents near the end of the month.

And, in good news the ANZ-Roy Morgan Consumer Confidence Index, while down slightly has stayed above a mark of 85 points for the sixth week in a row for the first time in two years. Commonwealth Bank projections expect a boost in sales for small businesses thanks to the Black Friday and Cyber Monday sales and the coming festive period.

Dollar cost averaging: can it work for you?

Australian share prices have seen record highs in 2024 after a sluggish couple of years.

The S&P ASX200 index added just under 7 per cent in the 10 months to October 31 closing at 8160.i It reached its previous all-time high of 8355 just two weeks before.

So, if you were invested in an index fund or a basket of shares mirroring the ASX200 for the entire period, it’s likely you would have added some value to your portfolio.

Over the course of the year, the index has ebbed and flowed, recording several all-time highs and some jarring notes in response to global events.

Geopolitical tensions have also played a part in market skittishness as the wars in the Middle East and Ukraine continue and economists argue about the future impact on Australia of a Trump presidency.

US share prices surged the day after Donald Trump’s election in what many saw as a positive reaction to the returning President’s policies. Since then, prices have declined in a not-unexpected correction. Various analysts are predicting future volatility as markets respond to the proposed policies including tariffs and mass deportations promised by the President-elect.

These ups and downs in prices can have investors scurrying to hit the ‘buy’ or ‘sell’ buttons. They may be desperate to save further losses when share prices are falling rapidly or wanting to cash in on a rising market. Meanwhile, those with lump sums to invest may delay, trying to pick the time when prices are lowest.

Timing the market

It’s a strategy – known as timing the market – that may work for some, particularly if you need access to your investment in the short term. But, for mid- to long-term investors, it’s generally accepted to be problematic.

To begin with, predicting the next market movement is extremely difficult – even for experienced investors – because of the endless factors that can influence the markets.

Reacting to major market movements by selling or keeping a lump sum in cash until ‘the time is right’ means you run the risk of missing the market’s best days and reducing your overall return.

Countless studies show that better long-term results are achieved by consistent investing over time.

In Australia, $10,000 invested in the ASX/S&P 200 during the 20 years to October 2024 would have increased to $60,777. ii But, if you had missed the 10 best days during that time, your total investment would be just $36,014.

Dollar cost averaging

One way of removing the emotion and guesswork is to consider investing at regular intervals over time, ignoring any market signals, in a strategy known as ‘dollar cost averaging’.

The strategy works best if you are investing over the medium to long term because it helps to smooth out the price peaks and troughs.

In fact, compulsory superannuation paid by employers is a form of dollar cost averaging. Smaller, regular amounts are invested automatically, regardless of market movements and, over time, the investment grows.

However, the jury is out on whether dollar cost averaging is a useful strategy when you have a lump sum in cash to invest.

Some advocates of dollar cost averaging argue that there’s a better return because you reduce the risk of making a large investment just before markets plunge.

Those opposed to the strategy for lump sum investing say that, with a lump sum sitting in a bank account as you chip away at regular stock purchases, there is a risk that you will miss the best of the market.

A 2023 study found that investing a lump sum in the markets at once over the long term delivers a better return than a dollar cost averaging strategy.iii

So, avoid the risks of timing the market and consider whether dollar cost averaging might be an appropriate strategy for you.

We’d be happy to discuss how best to ensure your regular investing strategy or investment of a lump sum, takes account of future market movements and volatility.

GST focus remains, while community tip-offs increase

Fraudulent claims for GST refunds continue to be a major focus for the ATO, with several new pilot programs announced to help small businesses with GST reporting.

Here’s a roundup of the latest tax news.

New PAYG adjustment factor

Pay As You Go (PAYG) instalments – whether you pay quarterly or twice-yearly – has been increased to 6 per cent for 2024-2025 to reflect the latest GDP increase.

The change in the adjustment factor does not affect taxpayers who work out their own instalments or pay annually.

PAYG instalment amounts can be varied through the ATO’s Online services for business if you believe your current instalment amount will be more or less than your expected tax liability for the year.

Pilot programs to protect GST system

The ATO will be running a number of pilot programs during 2025 that aim to improve the digital tax experience for small businesses.

The pilot programs will encourage more frequent payment and reporting by small businesses and try to reduce complexity by embedding the tax rules and logic into small business software.

The ATO also hopes to empower small businesses by providing more information to help them get their GST right from the start, providing them with more time to focus on their business, rather than their tax obligations.

Community tip-offs increasing

The community appears increasingly willing to report tax cheats. The ATO received more than 47,000 tip-offs during 2023-24, with around 90 per cent deemed suitable for further investigation.

Building and construction, cafes and restaurants, and hairdressing and beauty services topped the list of industries reported.

Common tip-offs include taxpayers not declaring income, demanding cash from customers, paying workers in cash to avoid paying tax and super, not reporting sales, and where someone’s lifestyle did not appear to match their income.

Obligations for festive season employees

Hiring new employees to help out during the festive season brings with it the same tax and super obligations as for regular employees.

The ATO is reminding employers to ensure they withhold the right amount of tax from any payments made and also to pay all eligible employees’ super funds the correct amount of Super Guarantee to avoid paying the Super Guarantee Charge.

Employers without an approved exemption, deferral or concession must lodge the necessary information for new employees through the Single Touch Payroll system from their first payday.

GST fraudster imprisoned

Stamping out GST fraud continues to be a priority for the ATO, with a Victorian woman sentenced to four years imprisonment after claiming nearly $600,000 in GST refunds from 27 fraudulent business activity statements.

She is also being pursued for the amount she fraudulently obtained by submitting the multiple false claims for a fake cleaning business.

The case is part of the ongoing ATO-led Operation Protego, which was set up in response to numerous cases of attempted GST fraud. So far 104 people have been arrested and 59 convicted.

Eligibility for small business litigation funding

If you have a dispute with the ATO being heard by the Administrative Review Tribunal, you may be eligible for litigation funding to cover “reasonable” legal expenses.

To qualify, you must be a small business (sole trader, partnership, company or trust) operating a business for all or part of the relevant income year and have a turnover under $10 million.

Funding is available only if the matter does not involve a tax avoidance scheme, fraud or cash economy issues. You must not have a history of failing to lodge tax returns.

Updating your ABN details

The ATO is reminding taxpayers holding an Australian Business Number (ABN) they need to regularly ensure their current contact details are correct so they don’t miss out on important help, information, or support like financial grants.

Check both your physical business address and postal address are listed on the Australian Business Register, together with your authorised contacts, contact details and business activities.

Gifting for future generations

At this time of year, when giving is particularly on our minds, some might turn their attention to how best share their wealth or an unexpected windfall with their loved ones.

You might be thinking about handing over a lump sum to help them with a major purchase or business opportunity, or be keen to help reduce or extinguish their student loans. Alternatively, it might be about helping to solve a housing problem.

Whatever the reason there are some rules that it is worth being aware of to ensure both you and they are protected.

Giving a cash gift

You can give anyone, family or not, a gift of cash for any amount and, as long as you don’t materially benefit from the gift or expect anything in return, no tax is paid on the amount by either you of the receiver.i

The same applies if you’re planning to pay out your child’s student loans.

However, be aware that if the beneficiary of your cash gift is receiving a government benefit, such as an unemployment benefit or a student allowance, there is a limit on the size of the gift they can receive without it affecting their payments.

They may receive up to $10,000 in one financial year or $30,000 over five financial years (which can not include more than $10,000 in one financial year).ii

Helping out with housing

Many parents also like to help their children get into the property market, where possible.

It’s been a difficult time for many in the past few years in dealing with the COVID-19 pandemic, the rising cost of living and interest rates, and a housing crisis.

A Productivity Commission report released this year found that while most people born between 1976 and 1982 earn more than their parents did at a similar age, income growth is slower for those after 1990.iii

With money tight and house prices climbing, three in five renters don’t believe they will ever own a home even though most (78 per cent) want to be homeowners, according data collected by the Australian Housing and Urban Research Institute (AHURI).iv

Just over half of those surveyed (52 per cent) were renting because they didn’t have enough for a home deposit and 42 per cent said they couldn’t afford to buy anything appropriate, the AHURI survey found.

So, in this climate, help from parents to buy a home isn’t just a nice-to-have it’s becoming a necessity for many.

Moving home

Allowing your adult child, perhaps with a partner and family, to share the family home rent-free is common option, giving them the chance to save up for a deposit.

One Australian survey found that one-in-10 people had moved back in with their parents either to save money or because they could no longer afford to rent.v

If it gets too much living under the same roof, building a granny flat in your backyard may be an option. Of course there are council regulations to consider, permits to be obtained and the cost of building or buying a kit but on the upside, it may add value to your home.

Becoming a guarantor

Another way to help might be to become a guarantor on your child’s mortgage. This might be the best way into a mortgage for many but before you sign, think it through carefully, understand the loan contract and know the risks.vi

Don’t forget that, as guarantor, you’re responsible for the debt. You will have to step in and repay if the lender can’t afford to repay, and the loan will be listed as a default on your own credit report.

Any sign that you are being pressured to be a guarantor on a loan may be a sign of financial abuse. There are a number of avenues for advice and support if you’re concerned.

It’s vital that you obtain independent legal advice before signing any loan documents.

If you would like more information about how to provide meaningful financial support to your children, we’d be happy to help.

Self managed super funds (SMSFs) can offer their members many benefits, but one that’s often overlooked is their potential as a multigenerational wealth creation and transfer vehicle.

Family SMSFs are relatively rare. According to the most recent ATO statistics (2022-23), the majority of SMSFs (93.2 per cent) have only one or two members.i Just 6.6 per cent have three or four members and only 0.3 per cent have five or six members (the maximum allowed).

Advantages of a family SMSF

An SMSF is sometimes established when two or more generations of a family share ownership or work in a family business. The fund can then form part of a personal and business succession plan, potentially making it easier to pass on ownership and management of assets to the next generation.

With more members, SMSFs also gain additional scale, allowing them to invest in larger assets (such as property). You can add business premises to the SMSF and lease it back without violating the related parties rule and 5 per cent limit on in-house assets.ii

Reduced tax and administration costs are also a benefit of multigenerational funds.

Running a family SMSF means the costs of establishing and administering the fund are spread across more members. This can be particularly helpful for adult children just beginning to save for their retirement.

In addition, more fund members means more people to share the administrative burdens of running an SMSF, which may be helpful as you get older.

A family SMSF does not need to be automatically wound up if you die or lose mental capacity and they can simplify the process of paying out a member death benefit as well as potentially allowing it to be paid tax-effectively. Note that death benefits paid to non‑tax dependent beneficiaries incur a tax rate of up to 30 per cent plus the Medicare levy.iii

More fund members also make setting up a limited recourse borrowing arrangement (LRBA) easier because their contributions reduce the fund’s risk of being unable to pay the borrowing costs. (An LRBA allows an SMSF to borrow money to buy assets)

Funding pension payments

Another advantage of an SMSF with up to six members may be when the fund begins making pension payments to older members.

If younger members are still making regular contributions, fund assets don’t need to be sold to make pension payments, which avoids the realisation of capital gains on assets.

Family SMSFs can also provide non-financial benefits, helping to transfer financial knowledge and expertise between the generations. And, while your children gain a solid financial education from participating in the running the SMSF, they can also provide valuable investment insights from a different perspective.

Risks and responsibilities

It is important to note that a multigenerational SMSF may not be right for everyone.

SMSFs of any size come with some risks and responsibilities. For example, if you lose money through theft or fraud, the government compensation that covers industry and retail super funds does not protect you. You are personally liable for the fund’s decisions, even if you act on advice from a professional, and your investments may not provide the returns you were hoping for.

Before you start adding your children and their spouses to your fund, it’s essential to spend time thinking about the challenges in running a family SMSF.

Fund members of different ages are at different stages in their retirement journey, with some accumulating savings and others drawing down.

This can make it tricky to administer and invest the fund’s assets in the best interests of all members.

For example, developing an asset allocation strategy catering to different life stages can be complex. Older members may prefer a strategy designed to deliver a consistent income stream, while younger members are usually more focused on capital growth.

Risk profiles are also likely to vary. Typically, younger fund members have a higher appetite for investment risk than members closer to retirement.

Family conflict can also be an issue when relationships are under pressure from divorce, blended families, and personality clashes.

The death of a parent can also create disputes over the distribution of fund assets or forced asset sales. Decisions about the payment of death benefits by the remaining trustees can derail carefully made estate plans and result in expensive legal battles.

Larger families with multiple adult children and partners may also find the six member limit an obstacle, forcing them to look at other options such as running a number of family SMSFs in parallel.

If you would look more information about establishing a family SMSF, call our office today.

10 questions to ask before setting up a family SMSF

How will decisions be made within the fund?

Will each member have an individual vote?

Will voting rights be proportional or in line with an individual member’s balance?

Will the voting system change as members’ balances increase (or decrease)?

Will children’s balances need to remain roughly equal, so they share equally in any asset growth?

How will the fund’s tax strategy cater for members with different incomes and ages?

How will deadlocks (such as over investment strategy) be overcome?

Who will take control if the key trustees die or becomes incapacitated?

How will the fund deal with the implications flowing from a member’s divorce?

What will happen when children have their own partners and children and want to leave and create their own SMSF?

Planning for what happens when you pass away or become incapacitated is an important way of protecting those you care about, saving them from dealing with a financial and administrative mess when they’re grieving.

Your Will gives you a say in how you want your possessions and investments to be distributed. But, importantly, it should also include enduring powers of attorney and guardianship as well as an advance healthcare directive in case you are unable to handle your own affairs towards the end of your life.

At the heart of your estate planning is a valid and up-to-date Will that has been signed by two witnesses. Just one witness may mean your Will is invalid.

You must nominate an executor who carries out your wishes. This can be a family member, a friend, a solicitor or the state trustee or guardian.

Keep in mind that an executor’s role can be a laborious one particularly if the Will is contested, so that might affect who you choose.

Around 50 per cent of Wills are now contested in Australia and some three-quarters of contested Wills result in a settlement.i

The role of the executor also includes locating the Will, organising the funeral, providing death notifications to relevant parties and applying for probate.

Intestate issues

Writing a Will can be a difficult task for many. It is estimated that around 60 per cent of Australians do not have a valid Will.ii

While that’s understandable – it’s very easy to put off thinking about your own demise, and some don’t believe they have enough assets to warrant writing a Will – not having one can very problematic.

If you don’t have a valid Will, then you are deemed to have died intestate, and the proceeds of your life will be distributed according to a statutory order which varies slightly between states.

The standard distribution format for the proceeds of an estate is firstly to the surviving spouse. If, however, you have children from an earlier marriage, then the proceeds may be split with the children.

Is probate necessary?

Assuming there is a valid Will in place, then in certain circumstances probate needs to be granted by the Supreme Court. Probate rules differ from state to state although, generally, if there are assets solely in the name of the deceased that amount to more than $50,000, then probate is often necessary.

Probate is a court order that confirms the Will is valid and that the executors mentioned in the Will have the right to administer the estate.

When it comes to the family home, if it’s owned as ‘joint tenants’ between spouses then on death your share automatically transfers to your surviving spouse. It does not form part of the estate.

However, if the house is only in your name or owned as ‘tenants in common’, then probate will probably need to be granted. This is a process which generally takes about four weeks.

Unless you have specific reasons for choosing tenants in common for ownership, it may be worth investigating a switch to joint tenants to avoid any issues with probate.

You will also definitely need probate if there is a refund on an accommodation bond from an aged care facility.

Super considerations

Another important consideration when dealing with your affairs is what will happen to your superannuation.

It is wise to complete a ‘binding death benefit nomination’ with your super fund to ensure the proceeds of your account, including any life insurance, are distributed to the beneficiaries you choose. You can nominate one or more dependants to receive your super funds or you could choose to pay the funds to your legal representative to be distributed according to your Will.

If a death benefit is paid to a dependant, it can be paid as either a lump sum or income stream. But if it’s paid to someone who is not a dependant, it must be paid as a lump sum.

If your spouse has predeceased you and you have adult children, they will pay up to 32 per cent on the taxable component of your super death benefit unless a ‘testamentary trust’ is established by the will, naming them as beneficiaries.

A testamentary trust is established by a Will and only begins after the person’s death. It’s a way of protecting investments, cash and other valuable assets for beneficiaries.

Rights of beneficiaries

Bear in mind that beneficiaries of Wills have certain rights. These include the right to be informed of the Will when they are a beneficiary. They can also expect to hear about any potential delays.

You are also entitled to contest or challenge the Will and to know if other parties have contested the Will.

If you want to have a final say in how your estate is dealt with, then give us a call.

Unexpected outcomes

David died in his early 60s. He left his estate to his wife Sally in accordance with his Will.

It seemed sensible at the time. But after a few years, Sally remarried. Unfortunately, the marriage did not last. When Sally died some 20 years later, her estate did not just go to her and David’s children but ended up being shared with her estranged second husband.

A testamentary trust, stipulating that the beneficiaries of both David’s and Sally’s estates were to be only blood relatives, may have solved this issue.

With heavy hearts we announce the passing of Peter Ferguson. As some of you are aware Peter had been unwell for some time which led to his retirement in 2020.

We cannot overstate his importance to both Dominion in his role as a financial planner and the service he provided our good clients. Everyone who was lucky to have worked with and alongside Peter will miss him.

We are sending our love and condolences to his wife, Barbara, and his family. Please think of them during this difficult time.

At this stage funeral arrangements have not been finalized, should you wish to be notified please contact the office.

Welcome to Spring, a season that might be motivational for personal, business and financial renewal. We hope you enjoy the sunshine and warmer weather.

Global stock markets – including the ASX – largely stabilised by the end of August after a turbulent month.

It was a rocky start when markets everywhere fell after news of high unemployment figures in the US and an interest rate move by Japan’s central bank. Despite the dramas, the S&P/ASX 200 closed 1.28% higher for the month marking a gain of just over 10% for the 12 months to date.

A slight drop in inflation figures – down to 3.5% in July from 3.8% the previous month – had investors checking the Reserve Bank’s reaction but most economists agree there’s no chance of an interest rate cut this year. The RBA’s not forecasting inflation to get to its preferred levels until late 2026 or early 2027.

While the cost of living has dropped ever so slightly (and partly due to $300 federal government rebates on electricity bills), wages have risen. The Australian Bureau of Statistics reports that wages rose by 4.1% in the year to June. It means that wages are now keeping up with the cost of living.

The good news from the markets and inflation data contributed to a small upswing in consumer confidence although there’s still much ground to recover after the losses caused by Covid-19.

How do retirement income options compare?

Retirement is filled with opportunities and choices. There’s the time to travel more, work on long-delayed personal projects or volunteer your help to worthwhile causes.

You also have a host of choices to make when it comes to funding your new life away from paid work. Here are four different options to consider.i

Account-Based Pension

An account-based pension (ABP) using your superannuation is one of the most common retirement income options. The amount you receive depends on the balance of your account and the drawdown rate you choose, subject to the minimum pension requirements set by the government.

Some considerations:

Tax benefits – Investment earnings, capital gains and withdrawals are tax-free, unless you have an untaxed component within your super.

Payment flexibility – Subject to pension minimums, most super funds allow you to adjust the payment amount and frequency, and even make partial or full lump-sum withdrawals if needed. You can also return to work and continue to receive a pension.

Longevity and market risks – You might outlive your account balance, especially if your withdrawals are high or your investment returns are poor.

Transition to Retirement

A transition to retirement (TTR) strategy allows access to some of your superannuation while still working, if you have reached age 60 (based on current rules).ii

Some considerations:

Flexible work options – You can reduce your working hours and supplement your income from your super.

Limits on pension rates – Similar to an ABP, there is a minimum annual pension rate. However, there is also a maximum annual withdrawal of 10 per cent of your TTR account balance.

Reduced retirement savings – Drawing on your superannuation while still working means your retirement savings might grow more slowly.

Annuities

An annuity is a financial product that provides a guaranteed income for a specified period or for the rest of your life. There are various types of annuities, including fixed, variable, and indexed annuities. You can purchase annuities or lifetime income streams using your superannuation.

Some considerations:

Predictable income – Provides a stable income stream, which can be reassuring for financial stability and provide an income for as long as you live.

Lack of flexibility – Once you purchase an annuity, the terms are generally fixed and you cannot alter the income amount. There’s a restriction on capital withdrawals or in some instances no access to capital at all.

Inflation risk – Fixed non-inflation-linked annuities may not keep pace with inflation unless specifically indexed to inflation.

Innovative Retirement Income Stream

An Innovative Retirement Income Stream (IRIS) is provided by a newer range of products. These were introduced after changes to regulations designed to deliver more certainty to retirement income by paying a pension for life without running out of funds.

Some considerations:

Age Pension benefits – Centrelink only counts 60 per cent of the pension payments received as assessable income and only 60 per cent of the purchase price of the product counts as an assessable asset until age 84 when it is reduced.

Certainty – Some IRIS products offer a stable guaranteed income stream, providing financial security.

No minimum requirements – IRIS products do not require an annual minimum amount, instead just requiring at least one annual payment.

Complexity – Features vary widely between different IRIS products and may involve complex terms or conditions.

Next steps

How do these different options suit your personal needs and how would they affect your retirement income? Consulting with a financial advisor can help you navigate these choices and tailor a plan that best suits your needs. Speak to us, so we can help you structure a plan to fund the retirement lifestyle you’ve worked so hard for.

Employers need to check that payroll systems reflect recent legislative changes, and the ATO is highlighting deduction opportunities available to some small businesses. Here’s your roundup of the latest tax news.

Updated employer obligations

The ATO is reminding employers to stay on top of legislative changes affecting payroll systems.

The Super Guarantee rate increased on 1 July 2024 to 11.5 per cent of ordinary times earnings, so all payments (starting with those for the July to September quarter) to super accounts for eligible workers must reflect the new rate.i

Individual income tax rate thresholds and tax tables changed also changed on 1 July 2024 so you may need to check calculations for your Pay As You Go Withholding obligations.

Claims for energy expenses

Many small business are eligible for a bonus 20 per cent tax deduction for new assets (or improvements to existing assets), that support more efficient energy usage.

The Small Business Energy Incentive applies to eligible assets first used or installed ready for use between 1 July 2023 and 30 June 2024.ii

Eligible expenditure for external training courses for employees incurred between 29 March 2022 and 30 June 2024 could also qualify for a 20 per cent bonus tax deduction from the Small Business Skills and Training Boost.iii

Pay less capital gains tax (CGT)

While a business can reduce capital gains made during a tax year by offsetting them with capital losses from the same or previous income years, not all capital losses are eligible.iv

Capital losses carried forward from previous years need to be used first, with losses from collectables (such as artwork and antiques) only permitted to be offset against capital gains from collectables.

Losses from personal use assets (such as boats or furniture), CGT exempt assets (such as cars and motorcycles), paying personal services income to yourself through an entity you set up, and leases producing income (such as commercial rental property), are ineligible as offsets.

Fuel tax credit rates change

Before claiming fuel tax credits in your next Business Activity Statement (BAS), check you are using the latest rates as they have changed twice in the new financial year.v

On 1 July 2024, the rate for heavy vehicles travelling on public roads changed due to an increase in the road user charge, with the rate altering again on 5 August 2024 due to a change in fuel excise indexation.

Different rates apply based on when you acquired fuel for your business’ use, so ensure you use the correct rate. If you are unsure, try the ATO’s online Fuel Tax Credit Calculator to work out the amount to report in your BAS.

Records essential for rental expense claims

Rental property investors without correct documentation to substantiate their expense deductions may find their claims declared invalid.vi

The ATO is warning investors they need all receipts, invoices and bank statements plus details of how deductions were calculated and apportioned for a valid claim.

Lodging a ‘nil’ BAS

While taxpayers registered for GST automatically receive a Business Activity Statement and are required to lodge and pay in full by the due date, businesses with nothing to report are still required to lodge.

If you have paused your business, you are required to lodge a ‘nil’ BAS by the due date either online or via the ATO’s automated phone service.vii

With the cost of doing business continuing to squeeze the bottom line, careful cash flow management has never been more important.

Not only is the ATO paying extra attention to timely payment of tax debts, but once the new payday super rules commence, many small businesses will no longer have access to one of their traditional sources of emergency funding.i

The government recognises how important cash flow is in small businesses and allocated an additional $23.3 million in the May 2024 Federal Budget to boost the adoption of eInvoicing. This electronic system is designed to help improve cash flow and productivity in smaller operations.

If you don’t have clear insights into your cash flow position and are not careful in managing income and expenses, it’s much harder to pay your bills and meet your tax, super and employer obligations.ii

A cash flow projection or budget helps to ensure there is enough cash available to meet upcoming expenditure. You will be able to understand your likely cash position at any time, identify fluctuations that could lead to potential cash shortages and plan for tax payments and major expenses.

The three main things to consider when creating a cash flow budget are timing, fixed and variable costs, and your income.

While cash flow projection tools can be off-the-shelf digital products or simple templates, we can also work with you to use the ATO’s Cash Flow Coaching Kit to improve management of this critical area.iii

Improving your position

When you have completed a cash flow projection and understand your position, it is time to work on ways to improve it.

One of the most important ways to improve cash flow is to ensure your invoices are paid as quickly as possible. Make sure invoices are sent out as soon as you can and, if possible, ask for immediate payment.

Consider shortening your payment terms, particularly if they are currently longer than 30 days. Some businesses offer an early payment discount or charge interest on overdue accounts to help speed up payments.iv

Setting clear payment guidelines for your customers is also valuable and think about taking action with customers who regularly fail to pay on time.

Review your payment cycle

Check suppliers’ payment terms to make sure you are not paying earlier than required (unless there is a discount on offer!).

Using a business credit card with an interest-free payment period can be an easy way to smooth your cash flow.

Separating your personal and business expenses makes tracking your business cash flow and expenses easier and reduces the time required for reconciliations.

Check stock levels

If you sell or supply products, carry out regular reviews of your inventory to ensure you are only holding the stock needed and are not tying up valuable cash flow and possibly increasing storage and insurance costs.

An inventory management system can be helpful to automate ordering and reduce lags between placing and receiving orders, and to identify unwanted or outdated stock.

Also review your pricing and margins to see if it is possible to raise prices without losing business.

Reduce your outgoings

Keeping a close eye on regular expenses and one-off spending helps to keep outgoings to a minimum.

Look for opportunities to save money by streamlining operations and reducing operating costs by cutting energy expenses and reviewing existing service contracts including phone and insurance.

Negotiating better prices with suppliers and more tightly targeting marketing expenditure can also boost your cash flow.

Make your asset work harder

If your business includes expensive assets like vehicles and equipment, ensure they are working hard for you.

Consider leasing or hiring assets to reduce upfront costs, sell assets you no longer need, and review any asset financing to make sure that it is competitive.

While these general tips may help improve your cash flow position, don’t forget we can provide advice tailored to the specific needs of your business. So, call us today if you would like our help.