As we come to the close of 2025, the team at Dominion would like to extend a sincere thank you for your continued support throughout the year. It’s been another big year, and we truly appreciate the trust you place in us.

With the festive season upon us, we’d also like to wish you and your loved ones a safe and Merry Christmas, and a happy and prosperous New Year.

Our office will close from 5pm on Friday 19th December 2025 and re-open Monday 12th January 2026 at 9am.

We look forward to continuing to work with you in 2026 and beyond.

With summer now upon us, it is the season of family gatherings, end of year celebrations, and holidays. We would like to wish you and your family a happy and safe festive season.

The economy came under renewed pressure in November as inflation accelerated. The first full monthly CPI release showed annual inflation rising to 3.8% in October, up from 3.6% the previous month. The Reserve Bank kept rates on hold in November and some economists are warning a rate rise may be on the horizon, possibly before the end of the year.

Despite the uncertainty, consumers may be getting their mojo back. The Westpac–Melbourne Institute Consumer Sentiment Index surged in November to its highest level since February 2022.

Unemployment eased a little to 4.3% in October after hitting a four-year high of 4.5% in September but wage growth remains higher, prompting concern from the RBA over the continued tight labour market.

Equity markets were volatile around the world thanks to uncertainty over the growing AI bubble, rising government debt and the ever-changing US tariff regime. Surging commodity prices halted the slide of the Australian dollar in the last week of the month with gold hitting record highs and iron ore prices holding firm. The Australian dollar hit a two-week high, finishing the month at $0.653.

Tax Alert December 2025

Getting ready for Payday Super and clearing up FBT myths

Big payroll changes are coming. From 1 July 2026 employers must pay super contributions at the same time wages, not quarterly. The ATO is also cracking down on fringe benefits tax (FBT) compliance, especially when it comes to work vehicles. Here’s what you need to know.

Payday Super: what employers must do

Employers will need to ensure they start preparing their payroll systems following the passing of the Treasury Laws Amendment (Payday Superannuation) Act 2025 on 4 November 2025.i

From 1 July 2026, employers will be required to make superannuation contributions for their employees at the same time as they pay their salary or wages, rather than quarterly as currently required.

More frequent super contributions will help employees’ super balances grow faster. But, for employers, it may affect cashflow by removing access to funds previously held until quarterly payments, so planning ahead is essential.

Small Business Clearing House closing

The ATO is again reminding employers that as part of the Payday Super reforms, the Small Business Super Clearing House (SBSCH) will close on 1 July 2026.

Although new users can no longer register to use the service, small businesses who are still using the SBSCH, need to begin transitioning to alternative services.

During the transition process, most employers will need to review their current software and payroll packages for super payment functions, or check the options offered by super funds, commercial clearing houses and payroll providers. If you are unsure of your options, you can contact us.

ATO’s compliance approach

The ATO has releaseddraft guidelinescovering its compliance approach during the first year of operation for the Payday Super legislation.

Employers will be classified into three risk zones, with the ATO prioritising its compliance resources on employers classified as being high or medium risk. The risk zone can change from pay period to pay period.

High risk employers will be those who have one or more ‘final individual SG shortfalls’ that have not been reduced to nil by the 28th day following the end of the quarter the qualifying earnings were paid, or if the employer is not otherwise in the low or medium risk zones.

Payroll governance in the spotlight

Small business employers are being encouraged to take a closer look at their payroll governance to check they are meeting their employer obligations in relation to taxes (PAYG, FBT), reporting (Single Touch Payroll) and super (SG and other super contributions).

According to the ATO, employers must have payroll governance measures that are effective and fit for purpose, which means having systems and processes tailored to their business’ structure, size, complexity and industry.

These systems should support the business to comply with its legal obligations and help it to identify and mitigate risks (such as administrative errors, employee fraud and cybercrime).

SMSFs and NPP readiness

From 1 July 2026, all SMSFs and super funds will need to ensure they can receive and allocate New Payment Platform (NPP) payments.

The NPP is a real-time payments platform used across Australia and it improves how quickly contributions can be received by employees’ super funds.

The changes mean SMSFs will be required to accept contribution payments and related data from employers via the super industry’s SuperStream standard, which uses a standardised electronic format.

Dual cab utes: FBT myths

Dual cab utes remain in the ATO’s sights as there is a common myth that employee use of these popular vehicles is automatically exempt from FBT.

However, the ATO is warning employers that providing a dual cab ute to an employee to complete their duties and also making it available for personal use may be subject to FBT.

For an employee’s personal use to be exempt, the vehicle must be both an eligible vehicle and only used for limited private use, meaning minor, infrequent or irregular use. FBT applies if the vehicle is used as the family taxi or for weekend personal trips.

If you need assistance implementing any of these changes before 1 July 2026 or you need a better understanding of how FBT works, reach out to us, we’re always here to help.

As the festive season approaches, there is a noticeable shift in the air. The days grow longer, school terms wrap up, and communities across the country begin to prepare for end-of-year celebrations in all kinds of ways.

For some, it is about unpacking boxes of decorations, preparing familiar family recipes and racing around the shops. For others, it is time to plan a beach day, host a casual BBQ, or simply enjoy a well-earned break from routine.

The festive season in Australia looks different for everyone. That’s part of what makes it so special. We live in a society full of rich cultural traditions. Some festive traditions have been passed down for generations, such as midnight Mass, lighting candles for Hanukkah, or gathering for a family meal on Christmas Day. Others have come to us through popular culture, often shaped by images of snowy winters and roaring fireplaces that don’t quite fit our sunny, southern hemisphere reality.

Think hot roast dinners in 35-degree heat, matching Christmas jumpers despite the sweat, and singing about snowmen and sleighbells.

And that’s okay. That’s part of the rich tapestry that is celebrating the festive season.

However, while tradition can be beautiful, it’s also worth asking yourself: do these traditions still bring joy to my life? Or am I doing them out of habit or obligation?

Reducing stress, reclaiming joy

The lead-up to the holidays can easily become overwhelming. This time of year often brings with it a long list of expectations about what to cook, how to decorate, where to be, and what to buy.

Trying to meet every expectation, real or imagined, can drain the joy right out of what is meant to be a time of celebration.

By letting go of pressure and embracing flexibility, we can shift the focus back to what really counts. Laughter. Connection. Rest. Reflection.

It is okay to opt out of what no longer fits. In fact, doing so often creates more space for what actually feels meaningful.

Rethinking what celebration looks like

While traditions can be a wonderful way to connect with our roots, they are not set in stone. Over time, life changes. Families grow and shift. Priorities evolve. The way we mark special moments can grow with us.

So, it is worth pausing to ask: are these traditions still adding joy to my life? Or am I continuing them out of pressure, or a sense of obligation?

Giving yourself permission to do things differently can be both freeing and fulfilling.

Making meaning in your own way

Reimagining tradition does not mean abandoning everything you love. It means choosing what feels right for you and creating space for joy, connection and rest – however that looks.

You might decide to swap the roast for prawns and salad and the pudding for a pavlova. Or ditch the mess of wrapping paper and presents in favour of shared experiences. You could even celebrate on a different day to reduce stress. Some people find joy in having a picnic in a beautiful location, taking a family beach walk at sunset, or simply spending the day unplugged from screens.

For others, creating new traditions might involve volunteering in the community or cooking dishes from their cultural heritage.

Whether your festive season is full of people or quiet moments, it only needs to reflect what matters most to you.

The season is yours to shape

There is no one way to celebrate. What is right for one person may not suit another and that is the beauty of it. The festive season does not have to look a certain way to be valid or joyful.

You might still love baking the same cake your grandmother made or singing carols in your street. Or you might find joy in starting completely new customs that reflect your values and lifestyle today. Either way, the important thing is that your celebrations feel true to you.

Small moments can become meaningful rituals too. A quiet morning coffee, a favourite song playlist, or calling someone you have not spoken to in a while are all things that can bring warmth and joy without adding stress.

Spring is here, bringing longer days and an opportunity to venture outdoors and enjoy the warmer months ahead.

A higher-than-expected jump in inflation figures may prompt the RBA keep interest rates on hold at this month’s meeting. Headline CPI climbed to 2.8%, up from 1.9%. The trimmed mean, the RBA’s preferred gauge of underlying inflation, also rose to 2.7% in July from 2.1% in June.

Markets responded cautiously, though the S&P/ASX 200 still edged higher for the month and notching another all-time high. The rally was driven by mining and banking stocks.

The unemployment dipped slightly to 4.2% in July and business confidence is upbeat. The number of Australian businesses rose by 2.5% over the past financial year to more than 2.7 million. Total wages and salaries increased 5.9 per cent year-on-year. The momentum appears to be lifting consumer sentiment with the Westpac-Melbourne Institute Index posting a solid gain 5.7% in August, a 3.5 year high.

As Aussie dollar finished the month at US65c and continues to be shaped by global factors.

In the US, the S&P 500 hit records highs, led by tech giants, as investors weighed tariff impacts and speculated on future rate cuts.

Strategies for an unexpected retirement

The best time to start planning for retirement is yesterday.

But the second-best time? Today.

About two-thirds of Australians retire earlier than they anticipated because of unexpected events such as job loss or redundancy, they need to care for a family member, have a sudden illness or injury, problems at work or a partner’s decision to retire.i

But, whether you’re in your 50s, 60s, or even beyond, it’s never too late to take meaningful steps toward a more secure and fulfilling retirement.

The good news is that with the right guidance and a few smart moves, you can still build a retirement plan that reflects your values, supports your lifestyle and gives you peace of mind.

Where to begin

Before you make any changes, it’s important to understand your current financial position. This includes:

your superannuation balance

other savings or investments

debts such as your mortgage, credit cards and personal loans

expected retirement income sources including the Age Pension, rental income and part-time work

Boost your super

Even if you’re starting later, there are ways to accelerate your super growth using:

Salary sacrifice Contributing pre-tax income into super can reduce your taxable income while boosting your retirement savings.

Personal contributions You may be eligible for a tax deduction or government co-contribution depending on your income.

Catch-up contributions You may be eligible to add to your super but be aware of the caps on contributions.ii

These strategies can be especially powerful in your 50s and 60s, when your income may be higher and retirement is on the horizon.

It’s also a good idea to regularly consider your super investment options and review your risk tolerance and time horizon.

Deal with debt

If possible, getting your debt under control before you retire is a useful strategy.

You could consider using your superannuation or other savings or downsize your home to pay off a mortgage or other loans. But first, it’s essential to carefully check the tax impact, the effect on your super and whether any potential government benefits will be affected.

Reassess your lifestyle goals

Retirement isn’t just about money, it’s about how and where you want to live, how much travel you’d like to do and if you’d continue to work part-time.

Clarifying your lifestyle goals helps shape your financial strategy. It also ensures your retirement plan reflects your values, not just your bank balance.

How much will I really need?

Aim to create a retirement budget. Estimate your future expenses including housing, food, travel and healthcare and compare them to your expected income. This helps identify any shortfalls and guides your savings strategy.

You will also need to consider the amount of time you might spend in retirement. This will depend on when you retire (planned or unexpected) and how long you live. This is called longevity risk. Given life expectancy is unpredictable, there is a possibility that your retirement savings may not last throughout retirement.

Understand your entitlements

Many Australians are eligible for government support in retirement, including:

Age Pension Based on income and assets, available from age 67 (for those born after 1957).

Concession cards For discounts on healthcare, transport and utilities.

Rent assistance If you’re renting privately and receive the Age Pension.

Even if you don’t qualify now, you may be able to restructure your finances to maximise future entitlements.

Review regularly and remain flexible

Retirement planning isn’t a one-time event. Life changes and so should your strategy. Regular reviews help you:

Adjust for market movements or legislative changes

Update your goals and spending patterns

Ensure your estate planning is current

Flexibility is key. Whether you retire gradually, take a sabbatical, or pivot to a new venture, your plan should evolve with you.

Next steps

Retirement planning is about taking the next step rather than chasing perfection. Whether you’re starting late or simply refining your strategy, every step you take now helps shape a more secure and meaningful future.

And remember that retirement isn’t an end point. It’s a new beginning even if you retire earlier than you anticipated. With the right plan in place, you can step into this next chapter with clarity, confidence and purpose.

We’d be happy to help you review your current retirement plan and identify any gaps in retirement goals and create a strategy should you need to retire earlier than expected.

While sweeping tax reforms aren’t expected this year, several targeted changes could affect your bottom line.

Tax debt no longer deductible

The ATO is reminding taxpayers the general interest charge (GIC) applied on an unpaid amount of tax or other liabilities after the due date is no longer tax deductible.i

The current rate applied to GIC debts is 11.17 per cent, with the interest charge compounding daily.

Prior to 1 July 2025, GIC could be claimed as a deduction in your tax return, but with the deduction no longer available, small businesses carrying any tax debts will now pay more.

Back pay reporting change

From the start of the 2025-26 tax year, the way that back payments to employees are treated and reported has changed.ii

In previous tax years, back payments accrued more than 12 months prior and exceeding $1,200 were reported at Lump Sum E in Single Touch Payroll (STP) reports.

The $1,200 threshold has now been removed, so all back payments accrued more than 12 months ago must be reported regardless of the amount.

Small Business Clearing House to close

The ATO’s Small Business Clearing House (SBCH) will shut down ahead of the new Payday Super regime launching 1 July 2026.iii

Small businesses with 19 or fewer employees could use the SBCH to pay their quarterly super contributions to the super funds selected by eligible employees.

The ATO says it will provide information to small businesses about transitioning to alternative super payment services, but businesses are being encouraged to take steps towards changing their payment arrangements before 1 July 2026.

Support for new small businesses

The ATO is providing extra support for new small business owners to help them understand and comply with their tax, super and registry obligations.

ABN holders will receive a series of emails with tips on their ABN obligations, business structure, registering for GST and employer responsibilities.

Focus on GST compliance

The ATO is also encouraging small businesses to set aside their GST payments in a separate bank account to avoid being caught out when it comes time to pay their obligations.iv

Compliance with GST registration and payment obligations remain an ongoing concern for the regulator, with the current annual tax gap estimated to be around $8 billion.

GST registration is compulsory when turnover exceeds $75,000 or if a business provides taxi, limousine or ride-sourcing services.

Notifying SMSF changes

SMSF trustees are being urged to ensure they notify the ATO whenever modifications are made to their SMSF.

Changes related to the fund’s contact details, structure, status or bank account must all be submitted to the regulator within 28 days.

Once the ATO receives the change details, the regulator will send an alert vis SMS or email to safeguard the SMSF against potential fraud or misconduct.

Work-related deductions continue to grow

Release of the annual Taxation Statistics Report for 2022-23 shows work-related expenses continue to dominate the tax deductions claimed by individuals, ensuring the ATO will maintain its current focus on this area.

Work-related expenses accounted for 50 per cent of individual deduction claims, with 10.3 million Australian taxpayers claiming an average of $2,739 per person in 2022-23.

Need help navigating the changes?

If any of these updates affect your business or personal tax situation, please contact us for help to understand your obligations, adjust your reporting processes and to plan ahead.

When you start researching for a trip overseas it’s easy to be swayed by what can be a lingering bad reputation of a region or country. The landscape of travel is constantly shifting and what may once have been a no-go zone can now be a dream destination – and vice versa.

Some of today’s most compelling places to visit were once dismissed as too dangerous, politically unstable, or simply unattractive. Thanks to urban renewal, political shifts, and the sheer resilience of local communities, these destinations have reinvented themselves and now welcome travellers with open arms.

Here are a few places that were once avoided but now deserve a spot on your bucket list.

Albania: Europe’s little secret

Let’s start with Albania. The once-hermit kingdom of Europe, it spent most of the 20th century shut off from the world under a dictatorship. Today? It’s a Mediterranean dream in disguise.

While tourists crowd into Italy and Greece, Albania’s beaches remain blissfully peaceful. The mountains are rugged, the food is incredible (think olive oil, cheese and stunning wines), and the prices? Almost suspiciously low. It’s a reminder that the best destinations are often the ones that haven’t been given the glossy treatment – yet.

And by going now, you’re not just ahead of the trend, you’re helping shape the nation’s tourism story from the ground up.

Rwanda: The quiet recovery

Few countries have flipped their narrative like Rwanda has. Once known for the horrors of the 1994 genocide, it is now one of Africa’s safest, cleanest, and most forward-thinking destinations. Kigali, the capital, is plastic-free, progressive, and is pulsing with creativity.

But the real magic lies beyond the city. Rwanda’s forests are home to some of the world’s last remaining mountain gorillas and tracking them in Volcanoes National Park is one of the most profound wildlife experiences on the planet. It’s not cheap, but every permit supports conservation and local communities so you can feel good about travelling with purpose.

There’s a quiet pride here and a sense of renewal. And for travellers, it offers that rare thing: a trip that’s humbling, hopeful, and unforgettable all at once.

Sri Lanka: The comeback island

Hop over to Sri Lanka, and you’ll find another country rising from the ashes of conflict and challenges. After decades of civil war, the 2004 tsunami, and an economic tailspin that led to widespread protests in 2022, the island nation has really started to shine as a holiday destination.

From leopard-spotting in Yala National Park to sipping world-class tea in the hill country, the island is a compact slice of paradise. The trains rattle their way through lush green hills, elephants roam wild, and its beaches are postcard perfect. Sri Lanka isn’t hiding its past; it’s simply writing a better future. It’s travel that feels good – and does good.

Vietnam: From conflict to cool

Vietnam is a nation that’s spun a difficult history into a compelling narrative. Once the setting for a war that defined an era, it’s now the backdrop for stunning cuisine and jaw-dropping natural beauty.

But what links Vietnam to places like Sri Lanka is its authenticity. The chaos of Hanoi’s Old Quarter, the sleepy magic of Hoi An, the emerald waters of Ha Long Bay all strike a chord when you remember just how far the country has come.

And yet, prices remain low and you can still find yourself the only tourist at a countryside café sipping egg coffee like a local.

The final boarding call

So, what do these places all have in common? They’re not perfect. And that’s exactly why they’re perfect. Destinations that have overcome hardship – be it conflict, natural disasters, or political upheaval – often offer something more rewarding than your average sun-and-souvenir spot.

These are places where your visit helps fuel recovery, where locals genuinely want to welcome you back, and where the scars of the past give way to a kind of hospitality you won’t find in more polished places.

So, skip the predictable and go where the stories are. Because sometimes, the best places to visit are the ones that were once off the map entirely.

Note: It’s crucial to stay informed about the current safety situation in any destination, even those that have undergone positive transformations.

Bonds are not usually the flashy upstarts of the investment world with their every move reported, like stocks.

But the Trump Administration’s extraordinary refashioning of world trade, with on-again off-again tariffs of eye watering amounts, has put bond markets in a similar position to share markets – in turmoil.

So, with the bond markets attracting more attention than usual, we take a closer look at the asset class.

What is a bond?

A bond is a bit like an interest-only loan and there are many different types of bonds available. A government (government bond), or sometimes a large company (corporate bond), issues bonds to investors to raise funds for infrastructure or, in the case of a company, for expansion.

Large institutional investors tend to favour some of the more complex types. Retail investors are more often interested in fixed-rate bonds, known as a fixed-income investment because of the regular payments made to the investor (or the coupon interest rate). The principal (called the face value) is repaid at an agreed date when the bond matures.

These bonds can also be traded on a secondary market by those who’ve chosen to sell their bonds before maturity. In this case, depending on the state of the markets and the economy, the amount they’re worth, or their capital value, may be higher or lower than the face value, which is fixed.

The most common fixed-rate bonds, issued by governments, are generally considered more stable. Nonetheless, all bonds are assigned a credit rating by independent rating agencies such as Standard & Poor’s or Moody’s.

Australia’s Commonwealth bonds, issued by the federal government, are AAA-rated reflecting strong fiscal management, economic stability and low default risk.i

State governments and quasi-government organisations such as the World Bank also issue bonds. The risk level for this category of bonds can vary.

Large companies, looking to expand or start new projects, often use bonds as a way to raise funds. Corporate bonds generally pay higher interest but are considered slightly more risky.

How to buy bonds

Investing in bonds can help to diversify a portfolio and provide a steady stream of income but for those with no knowledge or experience of the market, it is important to get quality professional advice and speak to us.

For example, if you had been relying on the conventional wisdom that bond markets are often up when share markets are down, recent share market activity would have delivered a shock. The usual flight to safety from share price volatility to bonds did not happen in the United States where, for a time, both markets were falling.

While it is possible to buy bonds directly when there is a public offer, it can be difficult for smaller individual investors to participate because of the large minimum transactions required.

Instead, most retail investors look to bond funds, bond exchange traded funds (ETFs) or managed funds for exposure to the bond market. The variety of funds on offer can help to diversify a portfolio by giving access to a range of different markets.

What affects bond rates?

Interest rate movements directly affect bond prices on the secondary market.

When interest rates rise, bond prices fall because newly issued bonds will be at the higher rate making older bonds less attractive and reducing demand.

Conversely, bond prices rise when interest rates fall because new bonds will offer the lower rates meaning there will be higher demand for older bonds, driving their prices up.

Bond prices are also influenced by economic conditions and investor sentiment.

Rising inflation can cause bond prices to rise while strong economic growth may decrease bond prices because investors often prefer to buy shares. Bonds with a lower credit risk, such as AAA-rated government bonds, tend to attract higher prices.

Be alert for scams

The Australian Securities and Investments Commission (ASIC) is warning investors about scammers using bond investments as a lure.ii

In one report earlier this year, scammers claimed to be offering sustainability investment bonds in Bunnings Warehouse.

The scam offered higher than market returns and claimed that investments are protected by the government. It included links to Bunnings genuine website although the company does not offer bonds or any investment products.

ASIC’s MoneySmart website warns that scammers often impersonate real companies. They may use the name of a real person working at the bank or company they say they represent.iii

“Be wary of surprise contact and independently verify who you are dealing with,” says ASIC. For detailed steps, see check before you invest.

If you would like to learn more about your options for investing in bonds, please give us a call.

How do bond yields change?

When bond prices fall, yields rise because the fixed coupon rate represents a higher percentage of the lower price. Similarly, when bond prices rise, yields fall because the fixed coupon rate is then a smaller percentage of the higher price.

For example, suppose interest rates fall. New bonds that are issued will now offer lower interest payments.

This makes existing bonds that were issued before the fall in interest rates more valuable to investors, because they offer higher interest payments compared to new bonds. As a result, the price of existing bonds will increase. However, if a bond’s price increases it is now more expensive for a potential new investor to buy. The bond’s yield will then fall because the return an investor expects from purchasing this bond is now lower.iv

Much of the 2025 Federal Budget was already known, after a volley of pre-election spruiking for votes. But Treasurer Jim Chalmers had one surprise up his sleeve – $17 billion in tax cuts. The first round of cuts will kick in on 1 July 2026 and second round on 1 July 2027, saving the average earner $536 each year when fully implemented.

With the next Federal Election due to be called any day, the Treasurer named five priorities for his fourth budget: helping with the cost of living, strengthening Medicare, building more homes, investing in education, and making the economy stronger.

He called it a plan for “a new generation of prosperity in a new world of uncertainty” that would help “finish the fight against inflation”.

The big picture

The Budget deficit has made an unwelcome, but not surprising, return. The Albanese government has been clear that we were headed back into the red and Treasurer Chalmers says the $42.1 billion deficit is less than what was forecast at both the last election and at the mid-year update.Gross debt has been reduced by $177 billion down to $940 billion, saving around $60 billion in interest over the decade.

Nonetheless, Australia is navigating choppy international waters with a “volatile and unpredictable” global economy.

Australia will feel the shockwaves from escalating trade tensions, two major global conflicts – in Ukraine and the Middle East, and slowing growth in China. Treasury predicts the global economy will grow by 3.25 per cent in each of the next three years in the longest stretch of below-average growth since the early 1990s.

However, Australia is in a good position to deal with the difficult conditions, the Treasurer says.

The Australian economy has “turned a corner” and continues to outperform many advanced economies.Inflation has moderated “significantly”, and the labour market has outperformed expectations. Meanwhile growth is predicted to increase from 1.5 per cent to 2.5 per cent by 2026-27.

Addressing the cost of living

With the rising cost of living expected to be central to the upcoming election campaign, the Budget aims to deliver more support to those doing it tough with further tax cuts, changes to Medicare and the Pharmaceutical Benefits Scheme (PBS), cuts to student debt and wage increases for aged care and childcare workers among a number of initiatives

Apart from the new tax cuts due in 2026 and 2027, the government will increase the Medicare levy low-income thresholds from 1 July 2024.

The energy bill relief is also being extended to the end of this year. At a cost of $1.8 billion, every household and around one million small businesses will each receive $150 off their electricity bills in two quarterly payments.

The government claims that energy bill relief has helped to drop electricity prices by 25.2 per cent across 2024.

Students aren’t forgotten in the Budget with a cut of $19 billion in student loan debt, with all outstanding student debts reduced by 20 per cent and a promised change to make the student loan repayment system fairer.

The government is tackling the cost of living where it’s often most obvious – at the cash register. It is providing support for fresh produce suppliers to enforce their rights and will make it easier to open new supermarkets. It’s also planning to focus on “unfair and excessive” card surcharges.

Looking for a clean bill of health

Almost $8 billion will be spent to expand bulk billing, the largest single investment in Medicare since its creation 40 years ago.

Treasurer Chalmers says nine-out-of-10 GP visits should be bulk billed by the end of the decade with an extra 4,800 bulk billing practices.

There’ll also be another 50 Urgent Care Clinics across the country, taking the total to 137, and public hospitals will get a boost of $1.8 billion to help cut waiting lists, reduce waiting times in emergency rooms and manage ambulance ramping.

Cheaper medicines

The cost of medicines is also in the government’s sights. The maximum cost of drugs on the Pharmaceutical Benefits Scheme (PBS) will be lowered for everyone with a Medicare Card and no concession card. From 1 January 2026, the maximum co-payment will be lowered from $31.60 to $25.00 per script and remain at $7.70 for pensioners and concession cardholders. Four out of five PBS medicines will become cheaper for general non‑Safety Net patients, with larger savings for medicines eligible for a 60‑day prescription.

An extra $1.8 billion is also being invested to list new medicines on the PBS.

Increasing the housing stock

The government’s previously announced target of 1.2 million new homes over five years has seen 45,000 homes completed in the first quarter.

The budget sees an extra $54 million to encourage modern construction methods and $120 million to help states and territories remove red tape.

With building set to increase, more apprentices are needed, and the government has announced financial incentives of up to $10,000 to encourage more people to take up apprenticeships in building trades. Some employers may also be eligible for $5,000 incentives for hiring apprentices.

The Help to Buy program that allows homebuyers to get into the market with lower deposits and small mortgages will be expanded with an extra $800 million to lift property price and income caps to make the scheme more accessible.

To help increase housing stock available, foreign buyers will be banned from purchasing existing dwellings for two years from 1 April 2025. Land banking by foreign owners will also be outlawed.

Recovering and rebuilding

The damage from ex-Tropical Cyclone Alfred and subsequent rains in Queensland and northern New South Wales is so extensive that it is expected to wipe a quarter of a percentage point off quarterly growth.

Flooding has damaged infrastructure and disrupted supply chains, agricultural production, construction, retail, and tourism activity.

The government expects costs of at least $13.5 billion in disaster support. As a result, the Budget includes $1.2 billion to be placed in a contingency fund to better respond to future disasters.

Looking ahead

Despite concerning events on the world stage, Australia’s economy is emerging “in better shape than almost any other advanced economy”.

Inflation and unemployment are coming down and wage growth will be stronger. To help underpin continuing economic growth, the Budget adds $22.7 billion to the government’s Future Made in Australia agenda.

It includes extra investment in renewable energies and low emissions technologies and an expansion of the Clean Energy Finance Corporation. The plan also includes more than $15 billion in support for private investment in hydrogen and critical minerals production, clean energy technology manufacturing, green metals, and low carbon liquid fuels.

And, as the trade war kicks off, the Budget allocates $20 million to a Buy Australian campaign.

“The plan at the core of this Budget is about more than putting the worst behind us. It’s about seizing what’s ahead of us,” the Treasurer says.

If you have any questions about the Budget measures announced, please don’t hesitate to contact us.

Information in this article has been sourced from the Budget Speech 2025-26 and Federal Budget Support documents. It is important to note that the policies outlined in this article are yet to be passed as legislation and therefore may be subject to change.

As we say goodbye to the heat of summer, we can look forward to enjoying the cooler days ahead. Along with the drop in temperature, the RBA brought much relief to mortgage holders and dropped the cash rate by 25 basis points in February. The cash rate is now sitting at 4.10 per cent following the first rate-reduction since November 2020.

Inflation remained steady in February, at 2.5 per cent and core inflation at 2.8 per cent; however, the RBA remains cautious and has not guaranteed further cash rate cuts in 2025. Some economists are predicting further cuts in 2025, but time will tell.

While there is ongoing tension between Russia-Ukraine and the Middle East, and a looming trade war due to Trump’s proposed tariffs, the global economic outlook continues to remain unpredictable.

US markets reacted to the lower-than-expected consumer spending and continued geopolitical issues, with another month of volatility.

It’s also been volatile on the Aussie share market, with the ASX 200 losing ground earlier in the month, bouncing back to reach an all-time high, only to start falling again to close at it’s lowest point in two months.

A similar pattern has been happening with the Aussie dollar, reaching a high of $0.64US cents mid-February, then losing momentum, and now hovering around $0.62US cents.

Turbocharge your super before 30 June

More than half of us set a new financial goal at the beginning of 2025, according to ASIC’s Moneysmart website. While most financial goals include saving money and paying down debts, the months leading up to 30 June provide an opportunity to review your super balance to look at ways to boost your retirement savings.

What you need to consider first

If you have more than one super account, look at consolidating them to one account. Consolidating your super could save you paying multiple fees and it will be easier to keep track of.

When transferring super into one account, do your homework and shop around, your current fund may not be your best option.i

How to boost your retirement savings

Making additional contributions on top of the super guarantee paid by your employer could make a big difference to your retirement balance thanks to the magic of compounding interest.

There are a few ways to boost your super before 30 June:

Concessional contributions (before tax)

These contributions can be made from either your pre-tax salary via a salary-sacrifice arrangement through your employer or using after-tax money and depositing funds directly into your super account.

Apart from the increase to your super balance, you may pay less tax (depending on your current marginal rate).ii

Check to see what your current year to date contributions are so any additional contributions you may make don’t exceed the concessional (before-tax) contributions cap, which is $30,000 from 1 July 2024.iii

Non-concessional contributions (after tax)

This type of contribution is also known as a personal contribution. it is important not to exceed the cap on contributions, which is set at $120,000 from 1 July 2024.iv

If you exceed the concessional contributions cap (before tax) of $30,000 per annum, any additional contributions made are taxed at your marginal tax rate less a 15 per cent tax offset to account for the contributions tax already paid by your super fund.

Exceeding the non-concessional contributions cap will see a tax of 47 per cent levied on the excess contributions.

If you’ve had a break from work or haven’t reached the maximum contributions cap for the past five years, this type of super contribution could help boost your balance – especially if you’ve received a lump sum of money like a work bonus.

These contributions are unused concessional contributions from the previous five financial years and only available to those whose super accounts are less than $500,000.

There are strict rules around this type of contribution, and they are complex so it’s important to get advice before making a catch-up contribution.

Meanwhile, the fate of a proposed new tax, known as Division 296, applying to super balances over $3 million is still unknown. It has yet to be debated and go to a vote in the Senate.

Downsizer contributions

If you are over 55 years, have owned your home for 10 years and looking to sell, you may be able to make a non-concessional super contribution of as much as $300,000 per person – $600,000 if you are a couple. You must make the contribution to you super within 90 days of receiving the proceeds of the sale of your home.

Spouse contributions

There aretwo ways you can make spouse super contributions, you could:

split contributions you have already made to your own super, by rolling them over to your spouse’s super – known as a contributions-splitting super benefit, or

contribute directly to your spouse’s super, treated as their non-concessional contribution, which may entitle you to a tax offset of $540 per year if they earn less than $40,000 per annum

Again, there are a few restrictions and eligibility requirements for this type of contribution.

Get in touch for more information about your options and for help with a super strategy that could help you achieve a rewarding retirement.

New year, new rules: ATO’s 2025 focus areas for small businesses

The Australian Taxation Office has kicked off 2025 by announcing its major areas of interest when it comes to small businesses. It has also highlighted a tougher stance when it comes to super guarantee (SG) compliance and GST fraud. Here’s a roundup of the latest tax news.

deductions and concessions (non-commercial losses and small business CGT concessions)

incorrect use of business income (business money and assets used for personal use of benefit), and

businesses operating outside the system (GST registration and income for taxi, limousine and ride-sourcing services).

The ATO intends to review and publish quarterly focus themes to help small businesses work on fixing issues in these areas.

GST fraud warning

The ATO-led Serious Financial Crime Taskforce is warning businesses against trying to cheat the tax and super system by committing GST fraud, saying it is on the lookout for potentially fraudulent activities.i

New information shared between government agencies shows some businesses are using complex financial arrangements to disguise transactions with the aim of obtaining larger GST refunds.

The arrangements include false invoicing between related entities, deliberately misaligning GST accounting methods across a group, duplicating GST credit claims, and claiming for fake purchases.

Tax penalties increase

The cost of penalty units imposed by the ATO if you fail to meet your tax obligations has increased again, rising from $313 to $330 per penalty unit.ii

The new rate applies to infringements occurring on or after 7 November 2024. For example, the penalty for failing to keep or retain tax records as required is 20 penalty units (20 units x $330 = $6,600).

Other penalties apply to missed and late SG payments, individual and corporate SMSF trustees and GST when buying or selling new residential premises.

SG compliance under scrutiny

With more timely data now available from Single Touch Payroll reporting, SG reporting and payments have become a priority area for the ATO. It is reminding employers to keep good records, report accurately and pay their obligations on time.

As part of its firmer response towards non-payment of SG contributions, the ATO issued 8,710 director penalty notices relating to 6,500 companies during 2023-24.iii

Although the regulator found 92.4 per cent of employers paid their SG obligations without intervention, it still collected and paid $932 million in SG entitlements into the super accounts of 797,000 employees.

GST and fuel tax credit time limits

The ATO is encouraging businesses eligible for GST and fuel tax credits to claim their credits within four years of the due date of the earliest Business Activity Statement (BAS) where a claim could have been made.

Once the time limit passes, you are no longer eligible to claim the credits. Lodging an amendment to an original assessment or requesting a private ruling are not considered as claiming.

Old credits can be claimed in your next BAS (provided it is within the eligibility period), by lodging a revised BAS for the original period via ATO Online Services, or by lodging a valid objection during the time limit to preserve your entitlement to the credits.

Change to myGovID

The Australian Government’s digital ID app myGovID, used to access government services, has been renamed myID.

The app provides secure access to government services using your existing login details (including email address), with the identity strength remaining the same. Existing app users should find the app automatically updated on their smart device, or it can be manually updated from the Apple app store or Google Play.

The ATO is warning users that scammers are seeking to take advantage of the name change. Any message or email asking you to set up a new myID or reconfirm your details is a scam.

From the economy bending policies of Trump 2.0 to the growing strength of the far right in Europe, the new alliance between Russia and the United States, the wars in Ukraine and the Middle East, and the US President’s vow to upturn world trade rules, the markets are certainly navigating tricky times.

In recent months we’ve seen volatility in some areas but cautious optimism in others in a reflection of the hand-in-glove relationship between politics and markets.

Of course, economic policies, laws and regulations– think tax increases or decreases, new business regulations or even referendums – have a big effect on how investors allocate their portfolios and that impacts market performance.

In 2016, when the United Kingdom voted to leave the European Union, the UK pound plunged and more than US$2 trillion was wiped off global equity markets.i

In the following four years until Brexit was finally achieved in 2020, the FTSE 100 performed poorly compared to other markets as domestic and international investors looked elsewhere to avoid risk. While it has risen since a massive drop during the coronavirus pandemic, the exodus of companies from the London Stock Exchange continues with almost 90 departures in 2024.ii

Interest rate movements and any hint of political instability can also bring about a sell off or a rally in prices, with companies holding off on capital investment and causing economic growth to slow.iii

Global oil prices rose 30 per cent in 2022 when Russia invaded Ukraine causing European stock markets to plunge 4 per cent in a single day.iv Since then, oil prices have fluctuated and are now back to pre-war levels and gold has reached new heights as investors globally look for a safe haven from high geopolitical risks.

Do elections have an effect?

Elections, which almost always cause market disruptions during the uncertainty of the campaign period and shortly after the vote is known, have featured strongly in the past six months or so.

A review of 75 years of US market data has found that, while there may be outbursts of volatility in the lead up to the vote, there’s minimal impact on financial market performance in the medium to long term. The data shows that market returns are typically more dependent on economic and inflation trends rather than election results.v

Nonetheless, the noisy 2024 US Presidential campaign saw some ups and downs in markets during the Democrats’ upheaval and the switch to Kamala Harris as candidate. Donald Trump’s various policy announcements on taxes, immigration, government cost cutting and tariffs both buoyed and dismayed investors.

Analysis by Macquarie University researchers of the three days before and after election day found significant abnormal returns in US equities immediately after the vote.vi

But the surge was short-lived as investor sentiment fluctuated. Small cap equities with more domestic exposure experienced the highest returns while the energy sector also saw substantial gains, in anticipation of regulatory changes.

While currently the S&P500 and the Nasdaq have both gained overall since the election, there’s been extreme share price volatility.

How Australia has fared

Meanwhile, any impact on markets ahead of Australia’s upcoming federal election has so far been muted thanks to the volume of world events.

The on-again off-again US tariffs are causing more concern here for both policymakers and investors. Tariffs on our exports could mean higher prices and a drop in demand for our goods and services, leading to economic uncertainty.

In early February, the Australian share market took a dive immediately after President Trump’s announcement of tariffs on Mexico, Canada and China, wiping off around $50 billion from the ASX 200. They recovered slightly only to fall again later as the Reserve Bank cut interest rates. In the US, some tech companies delayed or cancelled their listing plans because of the volatility and uncertainty caused by the announcements.vii

Amid a turbulent start to 2025, most economists agree the markets are unlikely to hit last year’s 7.49 per cent achieved by the S&P ASX 200.

Reserve Bank of Australia governor Michele Bullock is similarly downbeat on the prospects for the year, saying uncertainty about the global outlook remains “significant”.viii

Please get in touch if you’re watching world events and wondering about the impact on your portfolio.

As investors grapple with uncertainty, keeping a cool head has never been more important.

“Time in the market, not timing the market” is a popular investment philosophy that emphasises the importance of staying invested over the long term rather than trying to predict short-term market movements. While markets can be volatile in the short term, historically, they tend to grow over time.

It’s a strategy that helps you avoid getting caught up in short-term market fluctuations or trying to predict where the market is heading.

With the recent market turbulence, from the global effects of US President Donald Trump’s administration to ongoing conflicts in Ukraine and the Middle East, savvy investors look beyond the immediate chaos to focus on strategies that encourage stability and growth over the long-term.

It’s a hallmark of the approach by the world’s most high-profile investor, Warren Buffet, who argues that short-term volatility is just background noise.

“I know what markets are going to do over a long period of time, they’re going to go up,” says Buffet.i

“But in terms of what’s going to happen in a day or a week or a month, or even a year …I’ve never felt it was important,” he says.

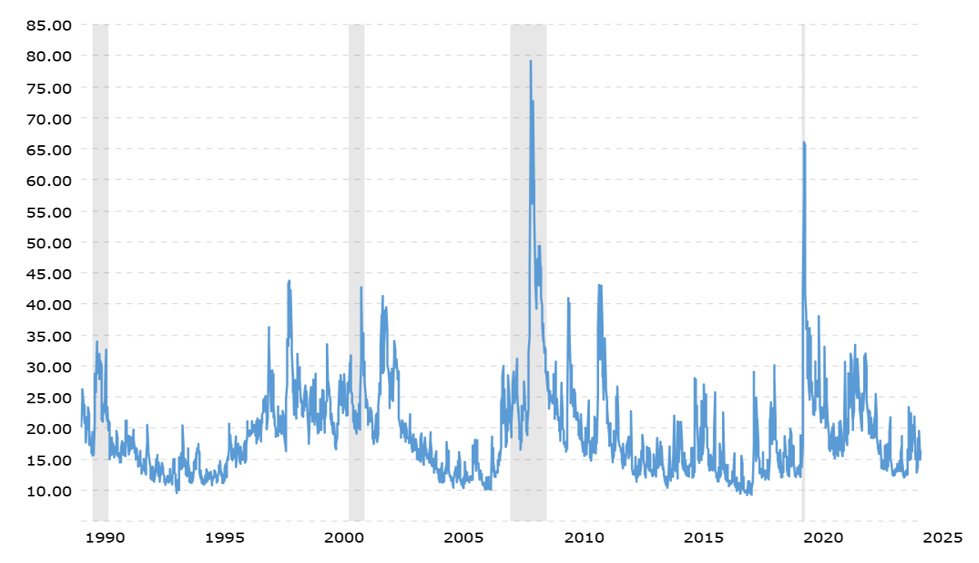

VIX Volatility Index – Historical Chart – 1990 -2025

Source: Macrotrends

Buffet first invested in the share market when he was 11 years old. It was April 1942, just four months after the devastating and deadly attack on Pearl Harbour that caused panic on Wall Street. But he wasn’t fazed by the uncertain times.

Today Buffet is worth an estimated US$147 billion.ii

Long-term growth in Australia

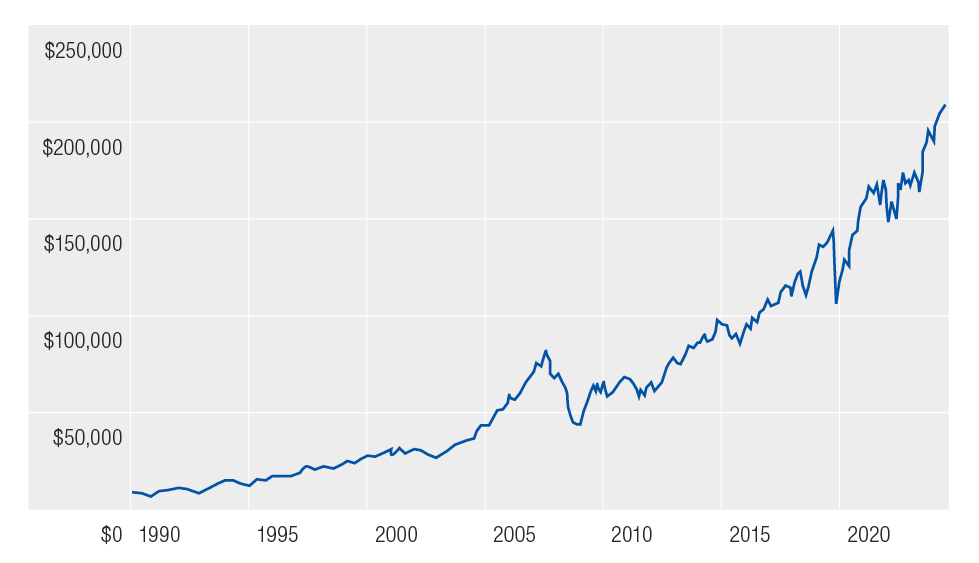

While growth has been higher in the US, investors in Australian shares over the long-term have also fared well. For example, $10,000 invested 30 years ago in a basket of shares that mirrored the All Ordinaries Index would be worth more than $135,000 today (assuming any dividends were reinvested).iii

And it’s not just the All Ords. If that $10,000 investment was instead made in Australian listed property, it would be worth almost $95,000 today or in bonds, it would be worth almost $52,000.

Australian shares – tracking performance from 1990 to 2024

Source: Vanguard

In real estate, the average house price in Australia 30 years ago was under $200,000. Today it is just over $1 milllion.iv

Meanwhile, cash may well be a safe haven and handy for quick access but it is not going to significantly boost wealth. For example, $10,000 invested in cash 30 years ago would be worth just $34,000 today.v

Diversify to manage risk

Diversifying your investment portfolio helps to manage the risks of market fluctuations. When one investment sector or group of sectors is in the doldrums, other markets might be firing, therefore reducing the chance that a downturn in one area will wipe out your entire portfolio.

For example, the Australian listed property sector was the best performer in 2024, adding 24.6 per cent for the year. But just two years earlier, it was the worst performer, losing 12.3 per cent.vi

Short-term investments – including government bonds, high interest savings accounts and term deposits – can play an important role in diversifying the risks and gains in an investment portfolio and are great for adding stability and liquidity to a portfolio.

Ongoing investment strategies

Taking a long-term view to accumulating wealth is far from a set-and-forget approach and by staying invested, you give your investments the best chance to grow, avoiding the risks of missing out on key growth periods by trying to time your buy and sell decisions perfectly.

Reviewing your investments regularly helps to keep on top of any emerging economic and political trends that may affect your portfolio. While it’s important to stay informed about market trends, it is equally important not to overreact when there is volatility in the share market.

Emotional investing can lead to poor decisions, so remember the goal is not to avoid market declines but to remain focussed on your overall long-term investment strategy.

Please get in touch with us if you’d like to discuss your investment options.

Welcome to summer and, for many, an active season with last-minute tasks and celebrations with family and friends. We take this opportunity to wish you and your family a joy-filled and safe festive season!

While headline inflation eased to 2.8% in the September quarter, the Reserve Bank remains unmoved on interest rates. RBA Governor Michelle Bullock says the drop in the cost of living may be welcome relief for most of us, but the Board’s measure to watch is trimmed mean inflation and that’s still not “sustainably” in the desired target range of 2-3%. It’s not likely to get there until late in 2026, the RBA predicts.

The sharemarket reacted sharply to the Governor’s comments in the last days of a month that had seen several all-time highs. US President-elect Donald Trump’s promise for 25% tariffs on Canadian and Mexican goods also contributed to the billion dollar shares sell-off. Nonetheless, the S&P ASX200 finished November 3.4% higher.

The Australian dollar is also taking a beating from the possibility of both the US tariffs and the RBA’s rates forecast. It hit a seven-month low below 65 US cents near the end of the month.

And, in good news the ANZ-Roy Morgan Consumer Confidence Index, while down slightly has stayed above a mark of 85 points for the sixth week in a row for the first time in two years. Commonwealth Bank projections expect a boost in sales for small businesses thanks to the Black Friday and Cyber Monday sales and the coming festive period.

Dollar cost averaging: can it work for you?

Australian share prices have seen record highs in 2024 after a sluggish couple of years.

The S&P ASX200 index added just under 7 per cent in the 10 months to October 31 closing at 8160.i It reached its previous all-time high of 8355 just two weeks before.

So, if you were invested in an index fund or a basket of shares mirroring the ASX200 for the entire period, it’s likely you would have added some value to your portfolio.

Over the course of the year, the index has ebbed and flowed, recording several all-time highs and some jarring notes in response to global events.

Geopolitical tensions have also played a part in market skittishness as the wars in the Middle East and Ukraine continue and economists argue about the future impact on Australia of a Trump presidency.

US share prices surged the day after Donald Trump’s election in what many saw as a positive reaction to the returning President’s policies. Since then, prices have declined in a not-unexpected correction. Various analysts are predicting future volatility as markets respond to the proposed policies including tariffs and mass deportations promised by the President-elect.

These ups and downs in prices can have investors scurrying to hit the ‘buy’ or ‘sell’ buttons. They may be desperate to save further losses when share prices are falling rapidly or wanting to cash in on a rising market. Meanwhile, those with lump sums to invest may delay, trying to pick the time when prices are lowest.

Timing the market

It’s a strategy – known as timing the market – that may work for some, particularly if you need access to your investment in the short term. But, for mid- to long-term investors, it’s generally accepted to be problematic.

To begin with, predicting the next market movement is extremely difficult – even for experienced investors – because of the endless factors that can influence the markets.

Reacting to major market movements by selling or keeping a lump sum in cash until ‘the time is right’ means you run the risk of missing the market’s best days and reducing your overall return.

Countless studies show that better long-term results are achieved by consistent investing over time.

In Australia, $10,000 invested in the ASX/S&P 200 during the 20 years to October 2024 would have increased to $60,777. ii But, if you had missed the 10 best days during that time, your total investment would be just $36,014.

Dollar cost averaging

One way of removing the emotion and guesswork is to consider investing at regular intervals over time, ignoring any market signals, in a strategy known as ‘dollar cost averaging’.

The strategy works best if you are investing over the medium to long term because it helps to smooth out the price peaks and troughs.

In fact, compulsory superannuation paid by employers is a form of dollar cost averaging. Smaller, regular amounts are invested automatically, regardless of market movements and, over time, the investment grows.

However, the jury is out on whether dollar cost averaging is a useful strategy when you have a lump sum in cash to invest.

Some advocates of dollar cost averaging argue that there’s a better return because you reduce the risk of making a large investment just before markets plunge.

Those opposed to the strategy for lump sum investing say that, with a lump sum sitting in a bank account as you chip away at regular stock purchases, there is a risk that you will miss the best of the market.

A 2023 study found that investing a lump sum in the markets at once over the long term delivers a better return than a dollar cost averaging strategy.iii

So, avoid the risks of timing the market and consider whether dollar cost averaging might be an appropriate strategy for you.

We’d be happy to discuss how best to ensure your regular investing strategy or investment of a lump sum, takes account of future market movements and volatility.

GST focus remains, while community tip-offs increase

Fraudulent claims for GST refunds continue to be a major focus for the ATO, with several new pilot programs announced to help small businesses with GST reporting.

Here’s a roundup of the latest tax news.

New PAYG adjustment factor

Pay As You Go (PAYG) instalments – whether you pay quarterly or twice-yearly – has been increased to 6 per cent for 2024-2025 to reflect the latest GDP increase.

The change in the adjustment factor does not affect taxpayers who work out their own instalments or pay annually.

PAYG instalment amounts can be varied through the ATO’s Online services for business if you believe your current instalment amount will be more or less than your expected tax liability for the year.

Pilot programs to protect GST system

The ATO will be running a number of pilot programs during 2025 that aim to improve the digital tax experience for small businesses.

The pilot programs will encourage more frequent payment and reporting by small businesses and try to reduce complexity by embedding the tax rules and logic into small business software.

The ATO also hopes to empower small businesses by providing more information to help them get their GST right from the start, providing them with more time to focus on their business, rather than their tax obligations.

Community tip-offs increasing

The community appears increasingly willing to report tax cheats. The ATO received more than 47,000 tip-offs during 2023-24, with around 90 per cent deemed suitable for further investigation.

Building and construction, cafes and restaurants, and hairdressing and beauty services topped the list of industries reported.

Common tip-offs include taxpayers not declaring income, demanding cash from customers, paying workers in cash to avoid paying tax and super, not reporting sales, and where someone’s lifestyle did not appear to match their income.

Obligations for festive season employees

Hiring new employees to help out during the festive season brings with it the same tax and super obligations as for regular employees.

The ATO is reminding employers to ensure they withhold the right amount of tax from any payments made and also to pay all eligible employees’ super funds the correct amount of Super Guarantee to avoid paying the Super Guarantee Charge.

Employers without an approved exemption, deferral or concession must lodge the necessary information for new employees through the Single Touch Payroll system from their first payday.

GST fraudster imprisoned

Stamping out GST fraud continues to be a priority for the ATO, with a Victorian woman sentenced to four years imprisonment after claiming nearly $600,000 in GST refunds from 27 fraudulent business activity statements.

She is also being pursued for the amount she fraudulently obtained by submitting the multiple false claims for a fake cleaning business.

The case is part of the ongoing ATO-led Operation Protego, which was set up in response to numerous cases of attempted GST fraud. So far 104 people have been arrested and 59 convicted.

Eligibility for small business litigation funding

If you have a dispute with the ATO being heard by the Administrative Review Tribunal, you may be eligible for litigation funding to cover “reasonable” legal expenses.

To qualify, you must be a small business (sole trader, partnership, company or trust) operating a business for all or part of the relevant income year and have a turnover under $10 million.

Funding is available only if the matter does not involve a tax avoidance scheme, fraud or cash economy issues. You must not have a history of failing to lodge tax returns.

Updating your ABN details

The ATO is reminding taxpayers holding an Australian Business Number (ABN) they need to regularly ensure their current contact details are correct so they don’t miss out on important help, information, or support like financial grants.

Check both your physical business address and postal address are listed on the Australian Business Register, together with your authorised contacts, contact details and business activities.

Gifting for future generations

At this time of year, when giving is particularly on our minds, some might turn their attention to how best share their wealth or an unexpected windfall with their loved ones.

You might be thinking about handing over a lump sum to help them with a major purchase or business opportunity, or be keen to help reduce or extinguish their student loans. Alternatively, it might be about helping to solve a housing problem.

Whatever the reason there are some rules that it is worth being aware of to ensure both you and they are protected.

Giving a cash gift

You can give anyone, family or not, a gift of cash for any amount and, as long as you don’t materially benefit from the gift or expect anything in return, no tax is paid on the amount by either you of the receiver.i

The same applies if you’re planning to pay out your child’s student loans.

However, be aware that if the beneficiary of your cash gift is receiving a government benefit, such as an unemployment benefit or a student allowance, there is a limit on the size of the gift they can receive without it affecting their payments.

They may receive up to $10,000 in one financial year or $30,000 over five financial years (which can not include more than $10,000 in one financial year).ii

Helping out with housing

Many parents also like to help their children get into the property market, where possible.

It’s been a difficult time for many in the past few years in dealing with the COVID-19 pandemic, the rising cost of living and interest rates, and a housing crisis.

A Productivity Commission report released this year found that while most people born between 1976 and 1982 earn more than their parents did at a similar age, income growth is slower for those after 1990.iii

With money tight and house prices climbing, three in five renters don’t believe they will ever own a home even though most (78 per cent) want to be homeowners, according data collected by the Australian Housing and Urban Research Institute (AHURI).iv

Just over half of those surveyed (52 per cent) were renting because they didn’t have enough for a home deposit and 42 per cent said they couldn’t afford to buy anything appropriate, the AHURI survey found.

So, in this climate, help from parents to buy a home isn’t just a nice-to-have it’s becoming a necessity for many.

Moving home

Allowing your adult child, perhaps with a partner and family, to share the family home rent-free is common option, giving them the chance to save up for a deposit.

One Australian survey found that one-in-10 people had moved back in with their parents either to save money or because they could no longer afford to rent.v

If it gets too much living under the same roof, building a granny flat in your backyard may be an option. Of course there are council regulations to consider, permits to be obtained and the cost of building or buying a kit but on the upside, it may add value to your home.

Becoming a guarantor

Another way to help might be to become a guarantor on your child’s mortgage. This might be the best way into a mortgage for many but before you sign, think it through carefully, understand the loan contract and know the risks.vi

Don’t forget that, as guarantor, you’re responsible for the debt. You will have to step in and repay if the lender can’t afford to repay, and the loan will be listed as a default on your own credit report.

Any sign that you are being pressured to be a guarantor on a loan may be a sign of financial abuse. There are a number of avenues for advice and support if you’re concerned.

It’s vital that you obtain independent legal advice before signing any loan documents.

If you would like more information about how to provide meaningful financial support to your children, we’d be happy to help.

Self managed super funds (SMSFs) can offer their members many benefits, but one that’s often overlooked is their potential as a multigenerational wealth creation and transfer vehicle.

Family SMSFs are relatively rare. According to the most recent ATO statistics (2022-23), the majority of SMSFs (93.2 per cent) have only one or two members.i Just 6.6 per cent have three or four members and only 0.3 per cent have five or six members (the maximum allowed).

Advantages of a family SMSF

An SMSF is sometimes established when two or more generations of a family share ownership or work in a family business. The fund can then form part of a personal and business succession plan, potentially making it easier to pass on ownership and management of assets to the next generation.

With more members, SMSFs also gain additional scale, allowing them to invest in larger assets (such as property). You can add business premises to the SMSF and lease it back without violating the related parties rule and 5 per cent limit on in-house assets.ii

Reduced tax and administration costs are also a benefit of multigenerational funds.

Running a family SMSF means the costs of establishing and administering the fund are spread across more members. This can be particularly helpful for adult children just beginning to save for their retirement.

In addition, more fund members means more people to share the administrative burdens of running an SMSF, which may be helpful as you get older.

A family SMSF does not need to be automatically wound up if you die or lose mental capacity and they can simplify the process of paying out a member death benefit as well as potentially allowing it to be paid tax-effectively. Note that death benefits paid to non‑tax dependent beneficiaries incur a tax rate of up to 30 per cent plus the Medicare levy.iii

More fund members also make setting up a limited recourse borrowing arrangement (LRBA) easier because their contributions reduce the fund’s risk of being unable to pay the borrowing costs. (An LRBA allows an SMSF to borrow money to buy assets)

Funding pension payments

Another advantage of an SMSF with up to six members may be when the fund begins making pension payments to older members.

If younger members are still making regular contributions, fund assets don’t need to be sold to make pension payments, which avoids the realisation of capital gains on assets.

Family SMSFs can also provide non-financial benefits, helping to transfer financial knowledge and expertise between the generations. And, while your children gain a solid financial education from participating in the running the SMSF, they can also provide valuable investment insights from a different perspective.

Risks and responsibilities

It is important to note that a multigenerational SMSF may not be right for everyone.

SMSFs of any size come with some risks and responsibilities. For example, if you lose money through theft or fraud, the government compensation that covers industry and retail super funds does not protect you. You are personally liable for the fund’s decisions, even if you act on advice from a professional, and your investments may not provide the returns you were hoping for.

Before you start adding your children and their spouses to your fund, it’s essential to spend time thinking about the challenges in running a family SMSF.

Fund members of different ages are at different stages in their retirement journey, with some accumulating savings and others drawing down.

This can make it tricky to administer and invest the fund’s assets in the best interests of all members.

For example, developing an asset allocation strategy catering to different life stages can be complex. Older members may prefer a strategy designed to deliver a consistent income stream, while younger members are usually more focused on capital growth.

Risk profiles are also likely to vary. Typically, younger fund members have a higher appetite for investment risk than members closer to retirement.

Family conflict can also be an issue when relationships are under pressure from divorce, blended families, and personality clashes.

The death of a parent can also create disputes over the distribution of fund assets or forced asset sales. Decisions about the payment of death benefits by the remaining trustees can derail carefully made estate plans and result in expensive legal battles.

Larger families with multiple adult children and partners may also find the six member limit an obstacle, forcing them to look at other options such as running a number of family SMSFs in parallel.

If you would look more information about establishing a family SMSF, call our office today.

10 questions to ask before setting up a family SMSF

How will decisions be made within the fund?

Will each member have an individual vote?

Will voting rights be proportional or in line with an individual member’s balance?

Will the voting system change as members’ balances increase (or decrease)?

Will children’s balances need to remain roughly equal, so they share equally in any asset growth?

How will the fund’s tax strategy cater for members with different incomes and ages?

How will deadlocks (such as over investment strategy) be overcome?

Who will take control if the key trustees die or becomes incapacitated?

How will the fund deal with the implications flowing from a member’s divorce?

What will happen when children have their own partners and children and want to leave and create their own SMSF?